LIT UPDATE & COMMENTARY

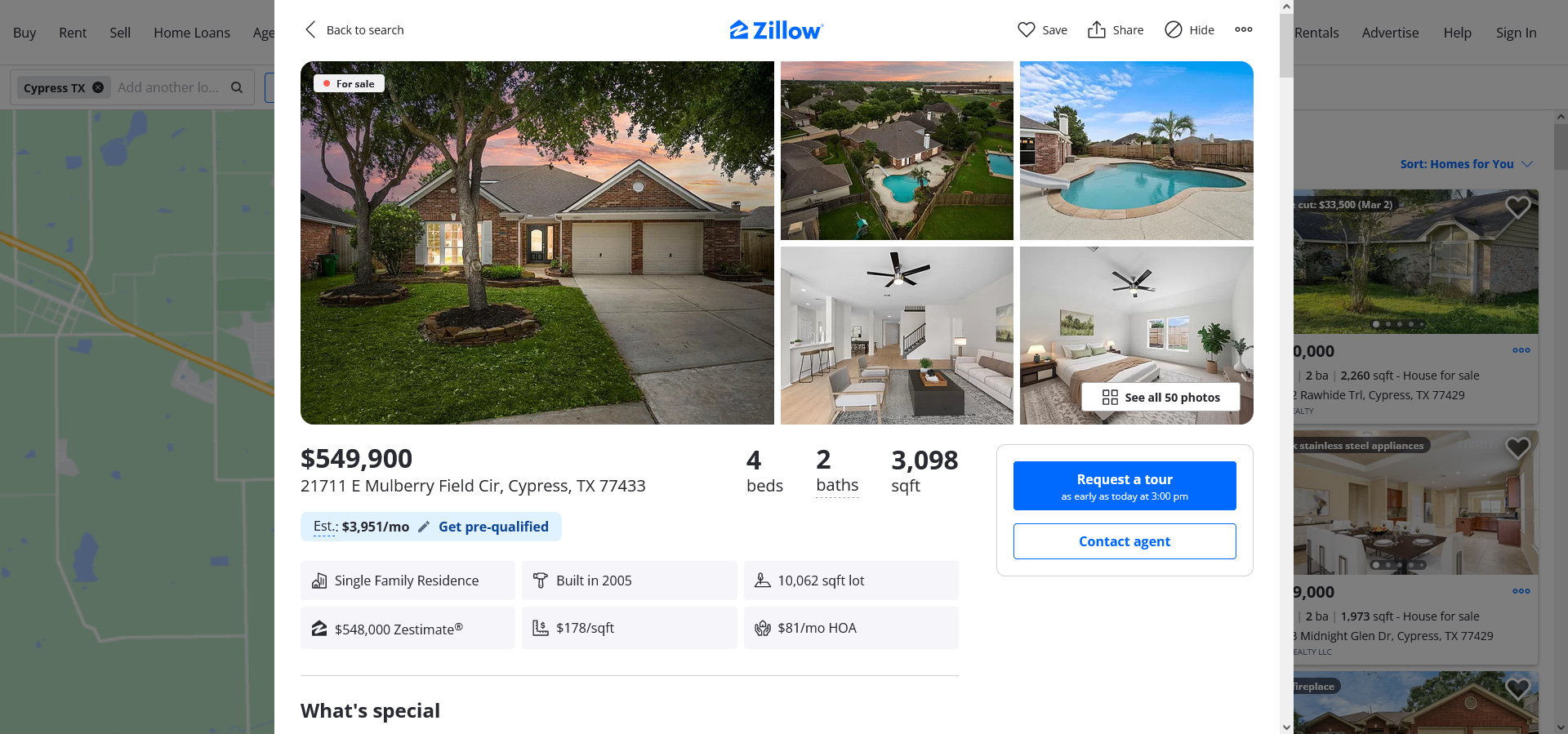

HUGE $100K PRICE DROP WITH ‘TENTATIVE’ UNDER CONTRACT SIGNAGE

Screenshot: Dec 14, 2024

LIT UPDATE & COMMENTARY

A LITTLE BIT OF BACKDATIN’ ON REAL PROPERTY RECORDS AND CASHIN’ IN ON CASH FOR KEYS

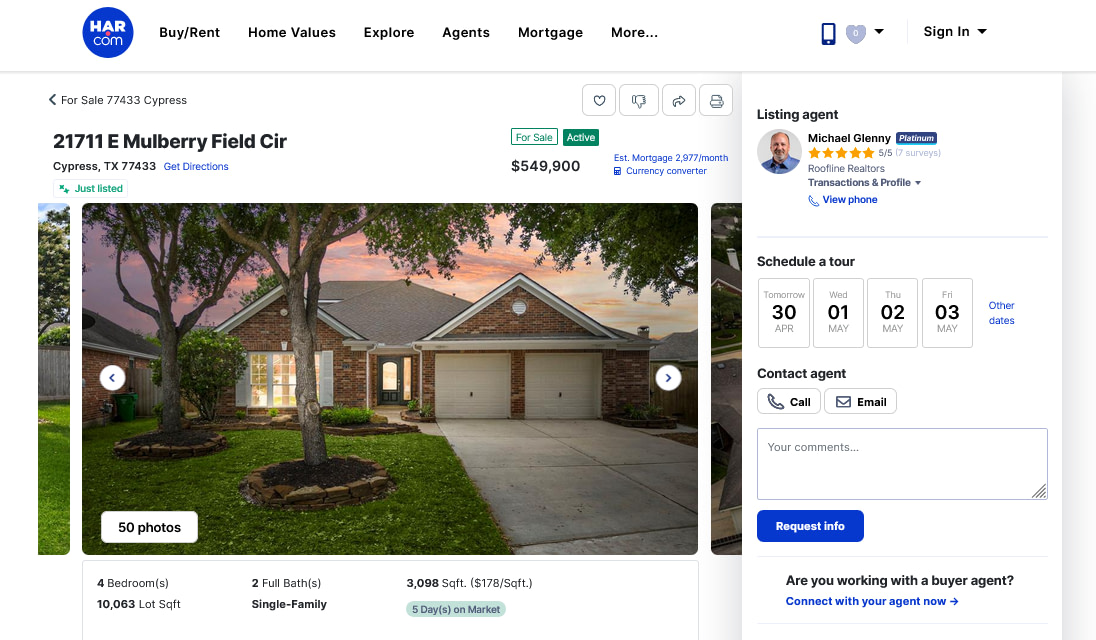

Screenshot: Jun 30, 2024 (only 4 days on the market, with a reduced price!)

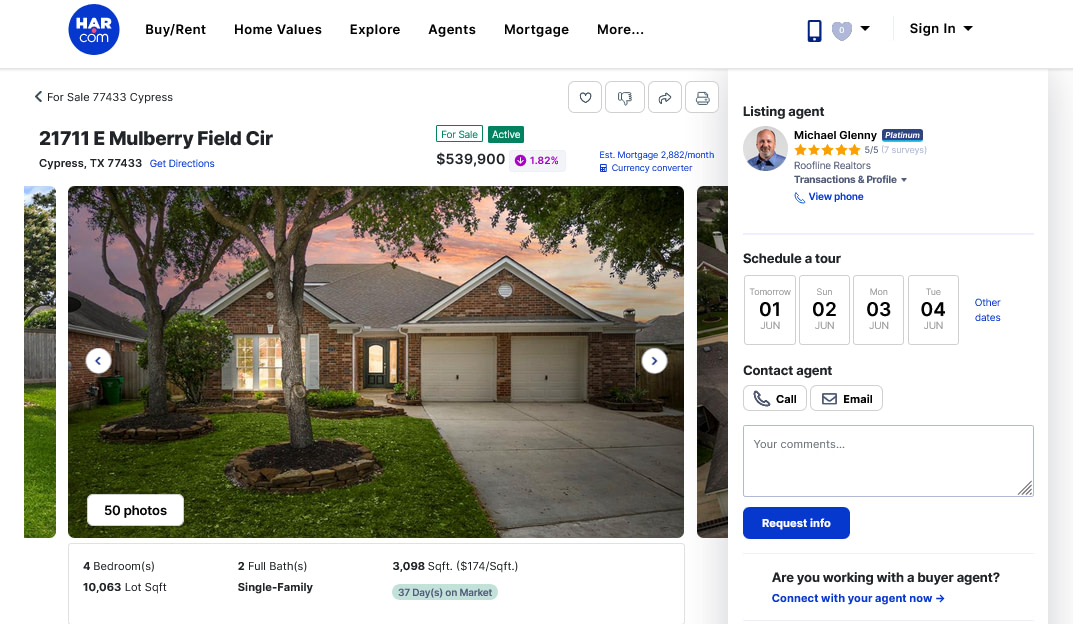

Screenshot: Jun 2, 2024

We’ve returned to update the shenanigans.

Not to be disappointed, we note that in real property records, the home at 21711 E Mulberry Field Cir, Cypress, TX 77433 has been transferred.

ZILLOW AND HAR

Here’s what Zillow’s take on ownership looked like prior to this update:

March 22, 2024: Home for sale by Auction.com (foreclosure).

Here’s today’s position: Home for sale privately.

HAR shows as at Apr. 29, 2024 the home’s been on the market for 5 days.

Update: As at May 31, its been on the market for 47 days. The price has been shaved down $10k to $539,900.

HARRIS COUNTY REAL PROPERTY RECORDS

There’s a new recording by a sanctioned realtor who’s entities include Gold Coast Equity LLC.

The date of this transfer is Feb 2, 2024 and the deed is signed on Jan. 31, 2024.

The transfer is from Gold Coast to Catamount Properties 2018, LLC, the Wall St owner of the original note.

The amount of the consideration. Legal tender of $10 bucks secures this nearly half million dollar home.

LIT never witnessed that recording previously and the fact the home has now come off the auction block and is for sale for $60k more leads us to deduce that our article highlighted the fraud and that Epiphany and Gold Coast would have to hand over the home to Catamount, and not sell it or transfer it again as they’ve done in cases like Dunn which we’ve also documented on LIT.

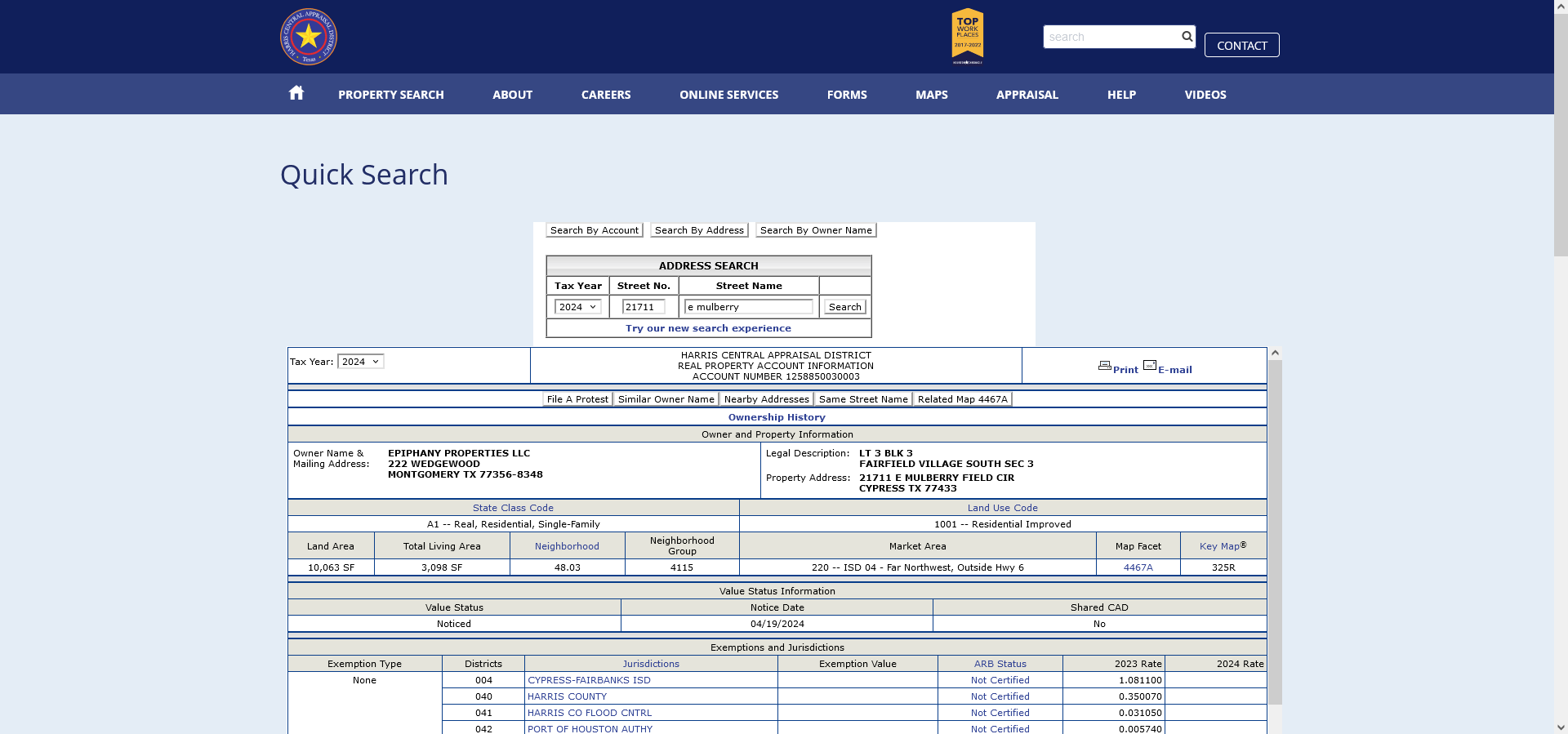

HCAD.ORG

As LIT previously confirmed, HCAD shows the transfer of Craig Mynard’s property to EPIPHANY PROPERTIES LLC.

There is no update reflecting any fraudulent transfer to Gold Coast on this website, although we noted the fraudulent $10 deed previously, recorded in real property records.

As at today, the view remains the same, with Epiphany proudly displayed as owners.

THE HOMESTEAD IS LISTED FOR $60K MORE THAN IT WAS A MONTH OR SO AGO

Zillow was selling for $490k in March and in April, the new owners are selling for $550k. That’s quite the price increase and ROI in one month (11 percent increase in gross sales value).

Maybe it will cover all those kickbacks for the blatant fraud we’ve documented.

We need to change the way the judiciary is structured and which is open for abuse and corruption due to no independent oversight or audits at either state or federal levels. https://t.co/zSRL3WSUMI

— lawsinusa (@lawsinusa) May 31, 2024

Mynard v. PennyMac Loan Services, LLC

(4:23-cv-04622)

District Court, S.D. Texas, Judge Kenneth Hoyt

DEC 12, 2023 | REPUBLISHED BY LIT: MAR 22, 2024

BEWARE OF COURT-CONTROLLED HOME THEFT FORECLOSURE SCAMS

The latest legal scam by CCTX, Epiphany, Kevin Pawlowski, Susan Casias, and Legal Bandits is a modified type of fraudulent contract and JV as LIT has witnessed with Rod Kagy’s My Fresh Start LLC: https://t.co/u3Esappren pic.twitter.com/Ix1KhxE8Wq— lawsinusa (@lawsinusa) March 22, 2024

This is disturbing on many levels, when you look at fellow foreclosure mill law firm and legal bandits BDF Hopkins who attacked foreclosure defense lawyer Robert Newark for practically the same reason but listed the new real property records: tfr to Kagy; https://t.co/qjkBWTdu4P

— lawsinusa (@lawsinusa) March 22, 2024

The Circle of Legal Bandits n Straw Men Entities we’ve highlighted include;

Christian Consultants of Texas (CCTX); Epiphany Properties LLC; ZP-1 Investments LLC, My Fresh Start LLC; My Foreclosure Hero (Vihn Truong); Momentum Title (Brian Brewer); Millennia Properties (Pasquale) pic.twitter.com/VjrakRwsEz— lawsinusa (@lawsinusa) March 22, 2024

UPDATE: RAPID DISMISSAL ARRANGED

“Specifically, the attorneys representing Freedom Mortgage Corp have neglected to address glaring evidence of real estate fraud and non-disclosure which contravenes the terms of the non-exempt property loan in question.” https://t.co/EzZN9CEAVc— lawsinusa (@lawsinusa) March 22, 2024

U.S. District Court

SOUTHERN DISTRICT OF TEXAS (Houston)

CIVIL DOCKET FOR CASE #: 4:23-cv-04622

| Mynard v. PennyMac Loan Services, LLC Assigned to: Judge Kenneth M Hoyt

Cause: 28:1332 Diversity-Notice of Removal |

Date Filed: 12/12/2023 Date Terminated: 01/11/2024 Jury Demand: None Nature of Suit: 290 Real Property: Other Jurisdiction: Diversity |

| Plaintiff | ||

| Craig James Mynard | represented by | Jason Andrew Leboeuf LeBoeuf Law Firm, PLLC 675 Town Square Boulevard Suite 200 Garland, TX 75040 214-206-7423 Fax: 214-730-5944 Email: jason@leboeuflawfirm.com LEAD ATTORNEY ATTORNEY TO BE NOTICED |

| V. | ||

| Defendant | ||

| PennyMac Loan Services, LLC | represented by | Helen Onome Turner Locke Lord LLP 600 Travis Street Suite 2800 Houston, TX 77002 713-226-1280 Fax: 713-229-2501 Email: helen.turner@lockelord.com LEAD ATTORNEY ATTORNEY TO BE NOTICEDKurt Lance Krolikowski Locke Lord LLP 600 Travis Street Suite 2800 Houston, TX 77002 713-226-1595 Fax: 713-223-3717 Email: kkrolikowski@lockelord.com LEAD ATTORNEY ATTORNEY TO BE NOTICEDThomas George Yoxall Locke Lord LLP 2200 Ross Aveune Suite 2800 Dallas, TX 75201-6776 214-740-8683 Fax: 214-740-8800 Email: tyoxall@lockelord.com LEAD ATTORNEY ATTORNEY TO BE NOTICED |

| Date Filed | # | Docket Text |

|---|---|---|

| 12/12/2023 | 1 | NOTICE OF REMOVAL from 334th Judicial District Court of Harris County, Texas, case number 2023-83412 (Filing fee $ 405 receipt number ATXSDC-30920480) filed by PennyMac Loan Services, LLC. (Attachments: # 1 Exhibit A, # 2 Exhibit B, # 3 Exhibit C, # 4 Exhibit D, # 5 Exhibit E, # 6 Exhibit F, # 7 Exhibit G, # 8 Exhibit H)(Turner, Helen) (Entered: 12/12/2023) |

| 12/12/2023 | 2 | CORPORATE DISCLOSURE STATEMENT by PennyMac Loan Services, LLC identifying PennyMac Financial Services, Inc. as Corporate Parent, filed.(Turner, Helen) (Entered: 12/12/2023) |

| 12/12/2023 | 3 | CERTIFICATE OF INTERESTED PARTIES by PennyMac Loan Services, LLC, filed.(Turner, Helen) (Entered: 12/12/2023) |

| 12/20/2023 | 4 | MOTION to Dismiss and Brief In Support by PennyMac Loan Services, LLC, filed. Motion Docket Date 1/10/2024. (Attachments: # 1 Exhibit A, # 2 Exhibit B, # 3 Proposed Order Granting Defendant’s Motion to Dismiss)(Turner, Helen) (Entered: 12/20/2023) |

| 01/02/2024 | 5 | ORDER for Initial Pretrial and Scheduling Conference by Telephone and Order to Disclose Interested Persons. Counsel who filed or removed the action is responsible for placing the conference call and insuring that all parties are on the line. The call shall be placed to (713)250-5613. Telephone Conference set for 2/15/2024 at 09:00 AM before Judge Kenneth M Hoyt.(Signed by Judge Kenneth M Hoyt) Parties notified.(CynthiaHorace) (Entered: 01/02/2024) |

| 01/10/2024 | 6 | STIPULATION of Dismissal / Joint Stipulation of Dismissal With Prejudice by PennyMac Loan Services, LLC, filed. (Attachments: # 1 Proposed Order of Dismissal)(Turner, Helen) (Entered: 01/10/2024) |

| 01/11/2024 | 7 | ORDER OF DISMISSAL. Case terminated on January 11, 2024. (Signed by Judge Kenneth M Hoyt) Parties notified.(JacquelineMata, 4) (Entered: 01/11/2024) |

| PACER Service Center | |||

|---|---|---|---|

| Transaction Receipt | |||

| 03/22/2024 09:38:42 |

Kenneth M Hoyt, presiding

Date filed: 12/12/2023

Date terminated: 01/11/2024

Date of last filing: 01/11/2024

TEXAS WAGONS ARE FULL OF LEGAL BANDITS IN 2024

Compare @statebaroftexas with @uscourts Turncoat and Bandit Texas Lawyer Jason Andrew Leboeuf’s Employer https://t.co/hI9Vu6UX5P pic.twitter.com/rZuQX7kjPj— lawsinusa (@lawsinusa) March 21, 2024

202383412 –

MYNARD, CRAIG JAMES vs. PENNYMAC LOAN SERVICES LLC

(Court 334)

Ancillary Judge Cory Sepolio Grants Disputed TRO and $5k Cash Bond for Three Properties With $50M Debt

The Order is overbroad because it enjoins Defendants from foreclosing for 64 days and violates Rule 680 of the Texas Rules of Civil Procedure.

Ronald Pugh’s House Thief is Kevin Pawlowski of Christian Consultants of Texas and Epiphany Properties

As the US Gov and State of Texas continue to double-down on the protection of an illegal housing theft scheme, CCTX’s Pawlowski keeps thievin’

House Thief Susan Casias of CCTX, Epiphany Properties, and Tech Box 21 is in Cahoots With Vilt n’ Ass.

As the US Gov and State of Texas continue to double-down on the protection of an illegal housing theft scheme, CCTX’s Casias returns.

KEVIN PAWLOWSKI

| Case (Cause) Number | Style | File Date | Court | Case Region | Type Of Action / Offense | |

|---|---|---|---|---|---|---|

| 202322179- 7 Ready Docket |

NGUYEN, MAI-LINH vs. CHRISTIAN CONSULTANTS OF TEXAS LLC | 4/6/2023 | 270 | Civil | Other Property | |

| 200618654- 7 Disposed (Final) |

ROJAS, MARIA L (FKA MARIA L CHAVEZ) vs. CHRISTIAN INVESTORS REAL ESTATE INC |

3/21/2006 | 334 | Civil | DTPA-DECEPTIVE TRADE PRACTICE | |

| 200577396- 7 Disposed (Final) |

FONVIELLE, CLAY vs. WHITAKER, ALANA | 12/8/2005 | 334 | Civil | CONVERSION | |

| 200257137- 7 Disposed (Final) |

CNP UTILITY DISTRICT vs. PAWLOWSKI, KEVIN (DBA AMERICAN INCOME LI |

11/4/2002 | 055 | Civil | Tax Delinquency | |

| 200106980- 7 Disposed (Final) |

CNP UTILITY DISTRICT (A POLITICAL SUBDIV vs. PAWLOWSKI, KEVIN (DBA AMERICAN LIFE INSU | 2/5/2001 | 234 | Civil | Tax Delinquency |

EPIPHANY PROPERTIES LLC

HOT OFF THE HARRIS COUNTY REAL PROPERTY RECORDS IS EPIPHANY AND GOLD COAST ACTUAL FRAUD UP NEXT FOLKS…. FILED FRIDAY, MAY 31, 2024. pic.twitter.com/1OujdiZo4c

— lawsinusa (@lawsinusa) June 2, 2024

SANCTIONED TREC/HAR REALTOR’S ENTITY GOLD COAST APPEAR TO BUY EPIPHANY’s FRAUDULENT CONVEYANCE…

JUN 2, 2024 UPDATE

Foreman v. Graham, 693 S.W.2d 774, 776 (Tex. App. 1985) (“Appellant intended to set this transaction up as a “Starker” exchange. To facilitate a tax-free transfer of the property, a Starker exchange, appellant wanted to assign the contract to a third party. The dispute arose over whether appellant would still be required by the sellers to sign the purchase money note, even though the earnest money contract would be assigned to a third party. Due to this dispute, the closing did not take place and both the buyer and the sellers, claiming the other had breached the contract, demanded the escrow funds.”)

Applying the Starker exchange, the contracts are legally infirm, but see;

202386606 – CHARLES, CLARENCE vs. STEPHENSON, NOVA-SHA

Citing to Judge Beau Miller and COA14

This allows fraudsters like Epiphany to “transfer” with nominal $10 value to Gold Coast and avoid litigation as shown in the Clarence case and also recently;

202377697 – VIZUET, BENJAMIN (JR) vs. FIDELITY NATIONAL TITLE AGENCY INC

As a p.s. Habitat know Gold Coast well and their property build division has closed deals in the past, some not so good when Nick Bhagia is involved…

201545054 – BUILT BY HABITAT LLC vs. GOLD COAST EQUITY LLC

The tax implications for each seller and buyer in this scenario can be complex and would depend on various factors such as the jurisdiction in which the property is located, the individual circumstances of each party involved, and any applicable tax laws and regulations. Here’s a general overview of the potential tax implications:

Seller 1 (Family of Deceased Homeowner):

The family of the deceased homeowner who sold the property to Buyer A (Epiphany) may need to report the sale on their tax return, especially if they inherited the property and its value increased from the time of inheritance to the time of sale. They may be subject to capital gains tax on the difference between the sale price and the property’s adjusted basis (which could be the fair market value of the property at the time of the homeowner’s death).

Seller 2 (Buyer A, Epiphany):

Buyer A (Epiphany), who sold the property to Buyer B (Gold Coast) for $10, might not incur any significant tax implications if they acquired the property and sold it shortly thereafter for a nominal amount. However, they might still need to report the transaction on their tax return and provide documentation of the sale.

Seller 3 (Buyer B, Gold Coast):

Buyer B (Gold Coast), who sold the property to Buyer C (Col Capitals) for $142,500 (loan amount), could potentially be subject to capital gains tax on the profit made from the sale. They would need to calculate the capital gain by subtracting the adjusted basis (which could be the purchase price plus any improvements made) from the selling price.

If Buyer B (Gold Coast) held the property for a short period before selling it, the gain might be treated as a short-term capital gain and taxed at ordinary income tax rates.

The tax liability on $142,500 of income for a single filer (personal) in the tax year 2024 would be approximately $34,647.52.

However, if they held the property for more than one year, the gain might be considered a long-term capital gain and taxed at lower capital gains tax rates.

Buyer C (Col Capitals):

Buyer C, who purchased the property for $142,500 and intends to use it as a rental property, may not have immediate tax implications related to the purchase itself. However, they would need to consider potential rental income tax, depreciation deductions, and other tax implications associated with owning and renting out the property.

If Buyers A, B, and C are Limited Liability Companies (LLCs), the tax implications can differ from those of individual taxpayers.

LLCs are typically treated as pass-through entities for tax purposes, meaning the income and expenses of the LLC “pass through” to the owners (also known as members) of the LLC, who report them on their personal tax returns.

However, LLCs can also elect to be taxed as corporations, which would change the tax treatment.

Here’s how the tax implications might vary for each party if Buyers A, B, and C are LLCs:

Seller 1 (Family of Deceased Homeowner):

The tax implications for the family of the deceased homeowner would likely be similar to those for individual sellers, assuming they are individuals and not an LLC. They would need to report any capital gains on the sale of the property on their personal tax returns.

Seller 2 (Buyer A):

If Buyer A is an LLC, the tax implications would depend on how the LLC is taxed. If Buyer A is a single-member LLC (owned by one individual), the sale might be treated similarly to an individual sale, with any capital gains reported on the owner’s personal tax return.

If Buyer A is a multi-member LLC, the tax implications would depend on the LLC’s operating agreement and tax structure.

Seller 3 (Buyer B):

Similar to Buyer A, if Buyer B is an LLC, the tax implications would depend on the LLC’s tax classification and structure. Any capital gains from the sale of the property would typically pass through to the members of the LLC and be reported on their personal tax returns, unless the LLC is taxed as a corporation.

Buyer C:

If Buyer C is an LLC, the tax implications would depend on the LLC’s tax classification and structure. Any rental income generated from the property would typically pass through to the members of the LLC and be reported on their personal tax returns. Expenses related to the rental property, such as maintenance and repairs, would also be deductible.

In summary, if Buyers A, B, and C are LLCs, the tax implications would depend on the tax classification and structure of each LLC, as well as the individual circumstances of the owners/members.

Take Advantage of Section 1031 of the Tax Code

What it is: IRS Section 1031 “like-kind” exchange

Who it’s for: Anyone who can reinvest the proceeds of rental property sales in new real estate

What you get: The ability to defer some or all taxes on the capital gain

Real estate investors can defer paying capital gains taxes using Section 1031 of the tax code, which lets them sell a rental property while purchasing a like-kind property and pay taxes only after the exchange is made. Legally speaking, the term like-kind is broadly defined. An investor need not swap out one condo for another or trade one business for another. As long as both properties in question are income-generating rental units, they’re fair game.

But timing is key with this method because investors have just 45 days from the date of a property sale to identify potential replacement properties, which they must formally close on within 180 days. And if a tax return is due (with extensions) before those 180 days, investors must close even sooner. Those who miss the deadline must pay full capital gains taxes on the sale of the original rental property.

Here’s some information about COL CAPITALS LLC:

COL CAPITALS LLC is a Texas Domestic Limited-Liability Company (LLC) that was filed on February 21, 2023.

The company’s filing status is listed as “In Existence,” and its file number is 0804936071.

The registered agent for the company is Republic Registered Agent LLC, located at 17350 State Hwy 249 Ste 220, Houston, TX 770641.

The managing members of COL CAPITALS LLC are Gabriel Fula Pinto and Juan Roa, both based in Houston, TX.

As a relatively new company, it has been in existence for approximately 1 year and 2 months.

Meet Darel I. Daik, we’re checkin this loan originator’s credentials as we review the fraudulence by Epiphany and Gold Coast, that sanctioned TREC/Har realtor’s shady entity. pic.twitter.com/G92u3XtfH9

— lawsinusa (@lawsinusa) June 2, 2024

STEPHEN AND ADRIANNA SCOTT

Original Loan of $69.5k in Stephen and Deborah (deceased) Scott’s name in 2004 (matures in 2034).

Home value $171k and Pawlowski offers $52k.

CHRISTIAN CONSULTANTS OF TEXAS (CCTX)

| Case (Cause) Number | Style | File Date | Court | Case Region | Type Of Action / Offense | |

|---|---|---|---|---|---|---|

| 202322179- 7 Ready Docket |

NGUYEN, MAI-LINH vs. CHRISTIAN CONSULTANTS OF TEXAS LLC | 4/6/2023 | 270 | Civil | Other Property | |

| 202313882- 7 Active – Civil |

CHRISTIAN CONSULTANTS OF TEXAS LLC vs. WILMINGTON SAVINGS FUND SOCIETY FSB (NOT IN IS INDIVIDUAL CAPACITY |

3/3/2023 | 333 | Civil | Debt / Contract – Other | |

| 202278191- 7 Disposed (Final) |

CHRISTIAN CONSULTANTS OF TEXAS LLC vs. SPRINGWOOD FOREST TOWNHOMES ASSOCIATION INC | 12/1/2022 | 234 | Civil | Debt / Contract – Debt / Contract | |

| 202080161- 7 Ready Docket |

AEL PROPERTIES LLC vs. HOWARD, KEIVOHN |

12/15/2020 | 055 | Civil | Other Property | |

| 201736615- 7 Disposed (Final) |

CHRISTIAN CONSULTANTS OF TEXAS L L C vs. CITIMORTGAGE INC | 6/1/2017 | 334 | Civil | OTHER CIVIL |

HOW DID AMY TRAN OBTAIN GOOD TITLE?

LIT HAS QUESTIONS ABOUT JUDICIAL FORECLOSURE SCAMS AND FRAUDS IN TEXAS

Question 1: Who’s livin’ at the property – as y’all servicers do drive-by inspection?

Question 2: Why did you not include the CCTX/Pawlowski filings in your 2024 case?@BNYMellon @GoldmanSachs @ecb @CFTC pic.twitter.com/Neg2XWQ6jP

— lawsinusa (@lawsinusa) March 23, 2024

202405020

– THE BANK OF NEW YORK MELLON (FKA THE BANK OF NEW Y vs. TAHA, TAMI

(Court 152, JUDGE ROBERT K. SCHAFFER)

Mackie Wolf’s recent filing in Harris County District Court regarding Tami Taha.

By way of background;

2015; Default 736 Judgment signed Feb 27, 2015

2019; BDF non-suited 736 for alleged COVID reasons

2021; BDF non-suited 736

2021; Tami Taha Loan Mod

2023; Zillow shows property “sold” on Mar. 16, 2023

2023; CCTX Record TREC Agreement recorded same day, Mar. 16, 2023 with sale amount $170k.

2023; HCAD shows CCTX as owners since Mar. 10, 2023.

2024; MW take over from BDF, filing a new 736 lawsuit on Jan. 26, 2024, seeking default Judgment with notice of hearing Mar. 28, Court 152, Judge Schaffer. There’s no mention of the recordings by CCTX/Pawlowski in your filings.

Now, according to the TREC agreement, Pawlowski provides moving boxes and one month’s rent to move out. The fact the service was returned undeliverable is a strong indication that she’s no longer in the property, which is most likely in control of Pawlowski et al.

Question 1: Who’s livin’ at the property – as servicers do drive-by inspection?

Question 2: Why did the foreclosure wolves not include the CCTX/Pawlowski filings in their 2024 case?

| Case (Cause) Number | Style | File Date | Court | Case Region | Type Of Action / Offense | |

|---|---|---|---|---|---|---|

| 202405020- 7 Active – Civil |

THE BANK OF NEW YORK MELLON (FKA THE BANK OF NEW Y vs. TAHA, TAMI | 1/26/2024 | 152 | Civil | Foreclosure – Home Equity-Expedited | |

| 202002227- 7 Disposed (Final) |

THE BANK OF NEW YORK MELLON (F/K/A THE BANK OF NEW vs. TAHA, TAMI |

1/14/2020 | 152 | Civil | Foreclosure – Home Equity-Expedited | |

| 201736624- 7 Disposed (Final) |

THE BANK OF NEW YORK MELLON F/K/A THE BANK OF NEW vs. TAHA, TAMI | 6/1/2017 | 152 | Civil | Foreclosure – Home Equity-Expedited | |

| 201472656- 7 Disposed (Final) |

GREEN TREE SERVICING LLC (AS MORTGAGE SERVICER FOR vs. TAHA, TAMI |

12/16/2014 | 152 | Civil | Foreclosure – Home Equity-Expedited | |

| 199559341- 7 Disposed (Final) |

TAHA, JAMALA vs. TAHA, TAMI | 12/11/1995 | 308 | Family | DIVORCE |

OR, did y’all pay @Ally the original $99.7k mortgage loan back from proceeds first? We’ll probably have to subpoena Dunn in due course to find out the real facts, coz y’all are playin’ monopoly in this real estate fraudulence endorsed by the Judiciary @uscourts @USAO_SDTX @FBI pic.twitter.com/D1PjIRIUSA

— lawsinusa (@lawsinusa) March 23, 2024

LIT AIN’T DUNN

Boston Homeowner Triumphs Against Foreclosure Rescue Scammers, Jury Awards Millions in Damages

Boston homeowner emerges victorious as a jury awards $2.75 million judgment against perpetrators of a foreclosure rescue scam.

Distressed Theft in Texas: The Real Victims of Home Theft Are a Soft Target for Officers of the Courts

If you’re a lawyer who doesn’t mind thievin’ or stealin’ real estate from distressed or elderly homeowners, become a lawyer or judge in Texas.

Distressed Theft in Texas: Fighting Back Against Fraudulent Mortgage Practices and Elder Abuse

LIT’s Ongoing Investigations Expose the Legal Culprits: Unraveling the Dark Web of Mortgage Fraud and Elder Abuse in Texas Courts.

More Weavin' Fraudulence

More Weavin' Fraudulence

The Sham Purchase of Dunn's Property

| Case (Cause) Number | Style | File Date | Court | Case Region | Type Of Action / Offense | |

|---|---|---|---|---|---|---|

| 202322179- 7 Ready Docket |

NGUYEN, MAI-LINH vs. CHRISTIAN CONSULTANTS OF TEXAS LLC | 4/6/2023 | 270 | Civil | Other Property | |

| 202313882- 7 Active – Civil |

CHRISTIAN CONSULTANTS OF TEXAS LLC vs. WILMINGTON SAVINGS FUND SOCIETY FSB (NOT IN IS INDIVIDUAL CAPACITY |

3/3/2023 | 333 | Civil | Debt / Contract – Other | |

| 202278191- 7 Disposed (Final) |

CHRISTIAN CONSULTANTS OF TEXAS LLC vs. SPRINGWOOD FOREST TOWNHOMES ASSOCIATION INC | 12/1/2022 | 234 | Civil | Debt / Contract – Debt / Contract | |

| 202080161- 7 Ready Docket |

AEL PROPERTIES LLC vs. HOWARD, KEIVOHN |

12/15/2020 | 055 | Civil | Other Property | |

| 201736615- 7 Disposed (Final) |

CHRISTIAN CONSULTANTS OF TEXAS L L C vs. CITIMORTGAGE INC | 6/1/2017 | 334 | Civil | OTHER CIVIL |

{kind=link}

{kind=link}

{kind=link}

{kind=link}