Bureau of Consumer Financial Protection v. Certified Forensic Loan Auditors, LLC

(2:19-cv-07722)

District Court, C.D. California

JUN 25

MARK BURKE AND JOANNA BURKE’S MOTION TO INTERVENE AND MOTION TO REOPEN CASE AS PLAINTIFFS AND MEMORANDUM OF LAW IN SUPPORT

Motion to Intervene

Proposed Intervenors, Mark Burke and Joanna Burke (“the Burkes”) contend that the intervention threshold is low (the threshold for intervention as a right under Federal Rule of Civil Procedure 24(a) is often considered low due to the rule’s focus on practical impairment of interests and liberal construction by the courts), and intervention is justified in this matter as their substantial interests are directly tied to the violations of the “suspended” judgment and settlement of this litigation. The Burkes respectfully renew their motion to intervene of right and to reopen this matter pursuant to Fed. R. Civ. P. 24(a)(2).

Procedural Compliance

The original motion was stricken for lack of conference. That procedural defect is now cured and the transcribed communication thread below is also provided as EXHIBIT 1 CONFER. The Burkes therefore submit this amended motion in full compliance with Local Rule 7-3.

A meet-and-confer with CFPB counsel was arranged for Tuesday, May 27, 2025 during which the Bureau refused to participate, refused to provide any legal position and Mark Burke for the Burkes was left frustrated despite his own transparency during the voice conference. Post-conference, it would take several email follow-ups to receive any meaningful responses from the CFPB. The first would be at 7.46 am CST on June 2, 2025: –

Mr. Burke, Thank you for the productive meet and confer conference on April 27. The Bureau does not consent to the proposed motion to reopen and intervene in Consumer Fin. Protection Bureau v. Certified Forensic Loan Auditors, LLC, et al., No. 19-07722, as the standards for intervention under Fed. R. Civ. Pro. 24 have not been satisfied. The proposed intervention is untimely and unwarranted, as the CFPB’s regulatory enforcement action was resolved in 2020, and bears no legal relation to Andrew Lehman’s private state court action for defamation. Any defenses to the claims in that action are properly presented in that forum, as appropriate. To the extent you have concerns for your personal safety and that of your mother, we encourage you to contact local law enforcement to address them. Sincerely, Gabriel Hopkins (Snr Counsel, CFPB).

Mark Burke responded at 11.06 am:

Good morning, Mr. Hopkins, Thank you for your response. After reviewing the details, I have a couple of questions regarding our recent phone conversation. First, addressing the “Affected Consumer” element: During our call, I informed you that Mr. Lehman explicitly admitted that Joanna Burke and John Burke qualify as “affected consumers” as defined in your stipulated judgment. Specifically, Paragraph 10 of the stipulated judgment states:“A judgment for monetary relief is entered in favor of the Bureau and against Defendants CFLA and Lehman, jointly and severally, in the amount of $3 million for the purpose of providing redress to Affected Consumers.” (emphasis added). Given this clear designation, what is your position on the refusal to grant an affected consumer access to financial redress? This is both a necessary and timely remedy. Second, regarding the claim of “untimeliness”: What is the intended purpose of a stipulated judgment that includes a five-year revocation period if there is no enforcement? To illustrate, consider an analogy we discussed during our call: Mr. Lehman was revoked [sic, arrested on motion to revoke] in Texas due to being in a stolen vehicle while in possession of, and under the influence of, a controlled substance—an incident that directly endangered his one-year-old child. This occurred alongside Ms. Monica Riley, who was also revoked and is now serving a five-year prison sentence. Does a stipulated five-year civil judgment not function in the same manner? For example, in CFPB v Prehired (adversary proceeding, Delaware Bankruptcy Court), there was also a stipulated final judgment issued in Case 23-50438-JTD, Doc 15, Filed 11/20/23. I look forward to your clarification on these matters. Sincerely, Mark Burke.

With no response after two reminders, at 1.31. pm CST on June 5, 2025, Mark Burke followed up with:

Good Afternoon Mr. Hopkins, Urgent Response Required – Conference & Prehired Precedent This marks the third formal request for your response regarding our conference. Your previous replies remain legally insufficient, and I now anticipate an immediate and professional response. Additionally, I have followed with great interest the recent communications concerning the Prehired adverse bankruptcy case. As I previously referenced, eleven states have ensured that affected consumers of predatory lending can obtain over $4 million in restitution. Yet, in these proceedings, you persist in denying such relief—even when supported by a California judgment. Notably:”Prehired was in bankruptcy and unable to issue refunds to its victims. In such cases, the CFPB’s Civil Penalty Fund is available to compensate harmed victims. See 12 C.F.R. § 1075.103. Our offices worked with the CFPB to secure an allocation from the Civil Penalty Fund, in the amount of $4,248,249. The CFPB finalized the allocation on May 30, 2024.” Now, the latest developments confirm that the CFPB, Mr. Vought, and President Trump, among others, are fulfilling this agreement—despite prior delays exceeding a year. I see no legal obstacle to our proposed intervention, which should secure identical relief. Given the clear precedent set by the Prehired settlement and the availability of the Civil Penalty Fund, our position is fully justified. I expect your timely response. Sincerely, Mark Burke.

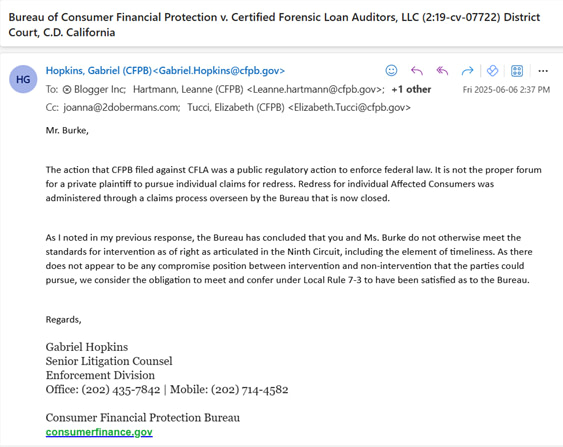

This triggered the final response from Mr Hopkins at 2.37 PM CST on Friday, June 6, 2025

Mr. Burke, The action that CFPB filed against CFLA was a public regulatory action to enforce federal law. It is not the proper forum for a private plaintiff to pursue individual claims for redress. Redress for individual Affected Consumers was administered through a claims process overseen by the Bureau that is now closed. As I noted in my previous response, the Bureau has concluded that you and Ms. Burke do not otherwise meet the standards for intervention as of right as articulated in the Ninth Circuit, including the element of timeliness. As there does not appear to be any compromise position between intervention and non-intervention that the parties could pursue, we consider the obligation to meet and confer under Local Rule 7-3 to have been satisfied as to the Bureau. Regards, Gabriel Hopkins, Senior Litigation Counsel, Enforcement Division

The Proposed Intervention Coincides With the “Dismantling” of the CFPB by the New Trump 47 Administration

The CFPB’s response to the Burkes intervention: “The Bureau does not consent to the proposed motion to reopen and intervene” is not a surprising statement in these proceedings, but most certainly an unlawful statement.

Since the new Trump 47 Administration has taken office:-

1. On Feb. 1, 2025 President Donald Trump fired Rohit Chopra, the director of the Consumer Financial Protection Bureau.

2. On Feb. 7, 2025, Elon Must posted on X: “CFPB RIP”.

See; https://lawsintexas.com/pr/3ya

3. On Feb 23, 2025 a 60 Minutes video confirms President Trump stating: “that was a vicious group of people running it [CFPB], they really destroyed a lot of people… President Trump then agrees with a reporter that he is trying to “eliminate” the CFPB as he is “trying to get rid of waste, fraud and abuse”.

See; https://lawsintexas.com/pr/3y8 [3 min 23 secs], last visited June 22, 2025.

4. On March 28, 2025, U.S. District Judge Amy Berman Jackson ordered a preliminary injunction that temporarily halted the Trump administration’s plan to lay off nearly 1,500 of the 1,700 employees at the Consumer Financial Protection Bureau. This order was appealed by the government. On April 11, 2025, the D.C. Circuit Court of Appeals issued a partial stay of the injunction. However, on April 28, 2025, the D.C. Circuit Court of Appeals reinstated the protection against layoffs, ensuring that employees could receive meaningful relief should the defendants not prevail in the appeal. The appeal of the preliminary injunction was later dismissed on May 7, 2025, as the order appealed from had expired by its own terms.

5. On May 6, 2025, 11 Attorney Generals wrote to the CFPB seeking enforcement and payment of $4.2M from the Civil Penalty Fund re Prehired. See; Burkes Email from Jun 5, 2025: Exhibit: Final-CFPB-Prehired-Letter-050625.pdf.

6. On June 5, 2025, California’s Dept of Financial Protection and Innovation said that the CFBP is now making good on a $4.2 million redress plan for former students of a shuttered sales-training firm following agency delays and subsequent pressure from various states.

7. On June 6, 2025, Mr Hopkins refused to engage in the Prehired settlement which was outlined in the email follow up from the Burkes on Jun 5, 2025.

8. On Jun 10, 2025 Cara Petersen, the Consumer Financial Protection Bureau’s acting enforcement director, resigned from the agency stating in part “I have served under every Director and Acting Director in the Bureau’s history and never before have I seen the ability to perform our core mission so under attack. It is clear that the Bureau’s current leadership has no intention to enforce the law in any meaningful way.”

See; https://lawsintexas.com/pr/3y9, ‘CFPB enforcement lead resigns, slams ‘attack’ on core mission in departure email’, CNN, last visited Jun 22, 2025.

9. On Jun 18, 2025, and as a direct result of the Burkes conference discussions with the CFPB, they “would restrict use of the fund to compensation for consumers impacted by companies subject to civil actions… In the 12 years since the rule was created, the CFPB has allocated $3.6 billion from the fund for “victims of activities for which civil penalties have been imposed under federal consumer financial laws.” See; https://lawsintexas.com/pr/3yb ‘CFPB Wants to Scale Back Use of Civil Penalty Fund’, PYMNTS, last visited Jun 22, 2025.

10. On Jun 20, 2025 ‘US Senate referee rules against cuts to CFPB, financial regulators in tax and spending bill’. See; https://lawsintexas.com/pr/3yd, Reuters, last visited Jun 23, 2025. Senate parliamentarian Elizabeth MacDonough, whose role is to ensure lawmakers follow proper legislative procedure, said a provision to effectively eliminate the budget for the CFPB could not be approved via a simple majority vote in the Republican-controlled chamber.

Defining Affected Consumers, Claims Processed and Suspended Judgments

The Bureau’s refusal to enforce its own “suspended” stipulated judgment in favor of “Affected Consumers” like the Burkes, while simultaneously reviving redress in CFPB v. Prehired under pressure from state attorneys general, exposes a troubling double standard: institutional actors are heard; pro se consumers are ignored.

Mr Hopkins disingenuous email on Jun 6, in part: “Redress for individual Affected Consumers was administered through a claims process overseen by the Bureau that is now closed.”. However, as lifted directly from the CFPB’s own press release (see; https://lawsintexas.com/pr/3yf, ‘Consumer Financial Protection Bureau Announces Settlement with Foreclosure Relief Services Company and its Owner’, Jul 20, 2020, there was no claims process, it was suspended.

This motion is accompanied by the memorandum in support herein and follows Fed. R. Civ. P. 24(c). The Burkes highlight the relevance of the prior CFPB settlement with CFLA and Lehman, closed in July 2020, as it pertains to this motion. The Burkes contend that the settlement and related litigation significantly impact their interests and form the basis for this intervention.

Judicial Notice

The Burkes request judicial notice of the cited cases and references to establish their relevance to this matter. This request is made pursuant to the standards outlined in Dorsey v. Portfolio Equities Inc., 540 F.3d 333, 338 (5th Cir. 2008), and Lee v. City of Los Angeles, 250 F.3d 668, 688-89 (9th Cir. 2001).

Motion to Reopen Case

The Burkes respectfully request this court reopen this ‘suspended judgment’ case. On June 20, 2020, there was an agreed settlement. As part of this settlement, there was a STIPULATED FINAL JUDGMENT AND ORDER AS TO CERTIFIED FORENSIC LOAN AUDITORS, LLC (CA), CERTIFIED FORENSIC LOAN AUDITORS (TX) AND ANDREW P. LEHMAN, Dkt 93 (July 20, 2020).

Specifically, Paragraph 10 of the stipulated judgment states: –

“A judgment for monetary relief is entered in favor of the Bureau and against Defendants CFLA and Lehman, jointly and severally, in the amount of $3 million for the purpose of providing redress to Affected Consumers.” (emphasis added).

Background Summary

This Action

On July 20, 2020, the United States District Court for the Central District of California entered a final judgment resolving the Consumer Financial Protection Bureau’s (CFPB) allegations against Certified Forensic Loan Auditors, LLC (CFLA) and Andrew Lehman (Lehman). The CFPB alleged that CFLA and Lehman engaged in deceptive and abusive practices, including false claims about their services and qualifications, and charging illegal upfront fees, in violation of the Consumer Financial Protection Act of 2010 (CFPA) and Regulation O. The court permanently banned CFLA and Lehman from the industry, imposed a suspended $3 million restitution judgment, and levied a $40,000 civil penalty.

The Burkes qualify as Affected Consumers because Joanna Burke and her late husband, John Burke, were former clients of CFLA and victims of its deceptive practices according to Lehman, and as admitted in court proceedings. See; Judge Gail Killefer’s Default Judgment Opinion signed Dec. 2, 2024 at p.5, #3.[1]

Mark Burke has been directly impacted by Lehman’s unlawful actions, which surfaced after the settlement’s publication in July 2020, necessitating this intervention to reopen the case and secure restitution for these unresolved harms.

Lehman’s Civil and Criminal History Relevant to this Motion

Andrew Peter Lehman has a lengthy documented history of criminal actions and ongoing vexatious civil litigation, underscoring a pattern of misconduct.[2]

On January 9, 2023, Lehman initiated a defamation lawsuit in Los Angeles Superior Court (23STCV00341)[3] against Mark Burke and the republication of a CFPB article on LawsInTexas.com about the underlying case. Despite being domiciled in Texas and under criminal court supervision and bond restrictions, Lehman filed as a pauper and was granted In Forma Pauperis (“IFP”) status.

A void default judgment was later entered on December 12, 2024, awarding Lehman and co-Plaintiff Monica Lynn Riley, now incarcerated to serve out a five-year jail sentence, $1,991,194.12 in damages and injunctive relief. Lehman has since sought to domesticate this judgment in Harris County District Court (202514896)[4].

The Burkes Connection and Relevance

Joanna Burke and her late husband, John Burke, have faced prolonged litigation stemming from predatory mortgage lending practices. Notably, they prevailed in Deutsche Bank National Trust Company v. Burke, S.D. Texas, (4:11-cv-01658) and continue to address related issues, with Joanna currently engaged in active litigation against PHH Mortgage Corporation.

Mark Burke, on the other hand, operates Blogger Inc. and publishes investigative journalism through LawsInTexas.com. His connection to the case arises from Lehman’s legal actions targeting his publication and the article regarding the CFPB settlement.

Lehman’s actions, directly affect the Burkes interests and underscore their need to intervene in the CFPB settlement case.

Memorandum of Law in Support of Intervention

Mark Burke is the proprietor of Blogger Inc., a nonprofit entity registered in Delaware and the legal blog LawsinTexas.com, which is dedicated to investigative journalism, particularly focusing on legal matters of public concern. To comprehend the significance, a brief overview is necessary. Behind every business stands an owner, entwined with a personal life. In Mark’s case, his digital media businesses facilitate a home office, doubling as his residence, which has been embroiled in prolonged litigation due to a predatory loan, which became the focus of a federal lawsuit, Deutsche Bank National Trust Company v. Burke (4:11-cv-01658) District Court, S.D. Texas, commenced Apr. 11, 2011. Legally owned by Joanna Burke, Mark’s mother, the property has hosted Mark’s home office since 2009.

John and Joanna Burke defeated Deutsche Bank twice in the 2011 proceedings, first at a bench trial in 2015 and again on remand in late December of 2017. However, Joanna Burke is still embroiled in an active civil suit against PHH Mortgage Corporation in Burke v. PHH Mortgage Corporation which relates to the 2011 proceedings.

At all times, the home remains the permanent residence of the Burkes.

Intervention Under Civil Rule 24(a)(2)

Federal Rule of Civil Procedure 24(a)(2) allows intervention as a right when an applicant claims an interest relating to the subject of the action and is so situated that the disposition of the action may, as a practical matter, impair or impede their ability to protect that interest, unless the existing parties adequately represent that interest. This language emphasizes the real-world impact of the litigation on the potential intervenor’s rights and interests. Courts construe Rule 24 “liberally” to allow parties with a legitimate interest to participate, resolving doubts in favor of proposed intervenors. The Burkes meet the requirements. The CFPB’s current presence does not protect that interest, rather it impedes the Burkes interests and is wholly inadequate.

Under the Federal Rules of Civil Procedure, Proposed Intervenor must satisfy four essential requirements for intervention: timeliness, a necessary interest, impairment of that interest without intervention, and the inadequacy of protection absent intervention (Fed. R. Civ. P. 24(a)(2)).

Necessary Interest

As explained above, the Proposed Intervenors have asserted their direct interest in the subject matter of the litigation, a necessary condition for intervention (Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001)).

This interest, related to the subject of the action, is legally protectable even if not enforceable, as per Wal–Mart Stores, Inc. v. Tex. Alcoholic Beverage Comm’n, 834 F.3d 562, 566 (5th Cir. 2016). Joanna Burke’s interests are as an “affected consumer” who has been subjected to stalking, as well as vile and harassing behavior by Lehman. He has made derogatory statements and has stalked her home while under strict supervision of Texas courts (wearing an ankle monitor). He and left repulsive statements on the front of documents left on her front door and created a website slandering her name and reputation and that of her deceased husband. These are detailed in related proceedings, listed herein, including Case No. 202311266 – KRUCKEMEYER, ROBERT J vs. BLOGGER INC D/B/A LAWIN TEXAS.COM (Court 152), Harris County District Court, Texas, Addendum L, Img # 108883355, 06/27/2023.

Mark Burke is intricately tied to Lehman due to his ongoing vexatious litigation targeting Mark Burke and his business interests. The imminent threat to his home office (residence) as a result of the latest legal maneuver by Lehman directly implicates his business, possessions, civil liberty, and constitutional rights.

As a result, the urgency of the Burke’s proposed intervention is evident in the intertwined personal, business, and legal battles. It is necessary that the Burkes obtain intervention in these proceedings as interested parties and affected consumer(s).

Timeliness of Intervention

This motion to intervene is timely, in alignment with the contextual nature of the timeliness inquiry (Sierra Club v. Espy, 18 F.3d 1202, 1205 (5th Cir. 1994)); California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006). This case involves a 5-year period tied to the suspended judgment and deferred penalties. The Burkes have filed this motion before that period expires. Their filing also follows Lehman’s attempt to domesticate a void judgment of nearly $2 million and his threats to foreclose on the Burkes residence, further emphasizing the urgency of their intervention.

Moreover, recent developments lend further weight to this motion. Following political changes after the 2024 election and the CFPB’s ‘deactivation’, enforcement efforts were significantly delayed or discontinued. Despite these challenges, the Ninth Circuit’s recent ruling in Consumer Financial Protection Bureau v. CashCall, Inc., No. 23-55259 (9th Cir. Apr. 24, 2025) confirms that judgments from prior CFPB actions remain enforceable, including restitution. Additionally, the Prehired settlement and June 2025 agreement for relief as discussed earlier only ratify the Burkes position.

Impairment of Interest Without Intervention

Without intervention, the Burkes substantial interests — including their rights to restitution and protection from further harm — would be significantly impaired.

Joanna Burke, a former client of CFLA and victim of Lehman’s deceptive practices, has a direct stake in the restitution outlined in the CFPB settlement.

Mark Burke faces ongoing litigation and direct challenges to his investigative journalism as a result of Lehman’s retaliatory actions, further underscoring the need to safeguard their rights. Adequate representation is lacking due to the CFPB’s current standing with the present administration, necessitating intervention to ensure their interests are preserved.

Intervention is crucial to safeguard these interests, as recognized in cases such as Atlantis Dev. Corp. v. United States, 379 F.2d 818, 828-29 (5th Cir. 1967). The Fifth Circuit has established that intervention is warranted when significant interests may be impaired without direct representation. Similarly, the Ninth Circuit in California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006), emphasized that intervention is appropriate where a party demonstrates a substantial interest that risks being impeded or impaired if intervention is denied, particularly when existing parties cannot adequately represent that interest.

The Burkes rights to restitution and protection from Lehman’s actions align with these principles, underscoring the necessity of intervention to ensure their interests are preserved.

Inadequacy of Protection Absent Intervention

The Burkes assert that their interests cannot be adequately protected without intervention. The CFPB, while instrumental in the original settlement, has demonstrated a lack of action in responding to the Burkes requests for assistance.

Relying on the CFPB’s 2020 settlement with CFLA and Lehman, the Burkes sought Lehman’s current address to address ongoing harassment and retaliatory actions against them. Despite detailing the harm caused by Lehman, including stalking, slander, vexatious litigation, and threats to their residence, the CFPB arranged a phone call with Mark Burke, but during this phone call declined to act on their behalf or provide a current address for Lehman, which had been requested to address these ongoing retaliatory actions.

This refusal emphasizes the CFPB’s inability or unwillingness to enforce the settlement terms, including securing restitution for affected consumers like Joanna Burke, as outlined in the $3 million judgment.

Mark Burke seeks intervention to ensure proper restitution and protect his financial interests. Lehman’s ongoing legal maneuvers — such as his efforts to domesticate a void $2 million judgment through litigation — further highlight the urgency of intervention to safeguard the Burkes rights.

These retaliatory actions directly impact the Burkes property, personal safety, financial well-being, and constitutional rights, necessitating representation beyond what the CFPB can offer.

Judicial precedents strongly support intervention under circumstances where existing parties fail to adequately protect substantial interests.

As established in Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001), intervention ensures that legally protectable interests are represented effectively.

Similarly, California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006) underscores that intervention is warranted when a party’s interests risk being impaired without direct involvement.

The Burkes unique position as affected consumers and subjects of Lehman’s retaliatory actions further demonstrate the inadequacy of protection absent their intervention.

The CFPB is No Longer a Consumer Watchdog under Trump 47 Administration

The conference between the Burkes and the CFPB highlights the precarious position of the Bureau. It is no longer a consumer watchdog under the current administration which ideally wanted to eliminate the Bureau. Whilst that has resulted in ongoing objections and rejections, a sampling of recent case dismissals by the CFPB support the Burkes position, and which the court may take judicial notice.

1. Consumer Financial Protection Bureau v. FirstCash Inc (4:21-cv-01251) District Court, N.D. Texas (ORDER: The Court STAYS all pending deadlines in this case and ORDERS that the Parties shall file the appropriate joint stipulation of dismissal with prejudice on or before July 14th, 2025. (Ordered by Judge Mark Pittman on 5/30/2025) (bdb) (Entered: 05/30/2025)).

2. Consumer Financial Protection Bureau (CFPB) v. Capital One, National Association (1:25-cv-00061), District Court, E.D. Virginia (Dismissed in a month – ORDER (Acknowledging Notice of Dismissal with Prejudice) – the Court hereby acknowledges this voluntary dismissal with prejudice, and with each party to pay its own costs and attorneys’ fees, and DIRECTS the Clerk’s Office to close the case. Signed by District Judge David J. Novak on 02/27/2025. (jlan) (Entered: 02/27/2025)).

3. Consumer Financial Protection Bureau v. Vanderbilt Mortgage and Finance, Inc. (3:25-cv-00004), District Court, E.D. Tennessee (Dismissed after 6 weeks: NOTICE of Voluntary Dismissal of case 3:25-cv-00004 by Consumer Financial Protection Bureau (Cater, Meghan) (Entered: 02/27/2025).

In conclusion, the CFPB has no desire to seek redress for the Burkes. However, the Burkes are legally entitled to redress in the absence of the Bureau’s assistance by this intervention.

Declaration

Pursuant to 28 U.S.C. § 1746, a litigant may submit an unsworn declaration in lieu of a sworn affidavit as evidence in federal court proceedings, including in opposition to summary judgment. See Nissho-Iwai Am. Corp. v. Kline, 845 F.2d 1300, 1305 (5th Cir. 1988) (‘Section 1746 allows a written unsworn declaration, subscribed as true under penalty of perjury, to substitute for an affidavit.’).

This principle has also been upheld in the Ninth Circuit. See Schwarzer, Tashima & Wagstaffe, Federal Civil Procedure Before Trial, § 14:131 (The Rutter Group 2025) (‘Unsworn declarations under penalty of perjury are permissible under 28 U.S.C. § 1746 and carry the same evidentiary weight as affidavits.’).

I, Mark Stephen Burke, my date of birth is June 20, 1967, residing at 46 Kingwood Greens Dr, Kingwood, Texas, 77339, declare under penalty of perjury under the laws of the United States of America that the information contained herein is true and correct.

I, Joanna Burke, my date of birth is November 25, 1938, residing at 46 Kingwood Greens Dr, Kingwood, Texas, 77339, declare under penalty of perjury under the laws of the United States of America that the information contained herein is true and correct.

Conclusion

For the foregoing reasons, the Burkes respectfully request that this Court grant their (i) motion to reopen the case and (ii) motion to intervene.

The Burkes meet all the legal requirements for intervention as established by relevant judicial precedents, including Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001), and California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006).

Their substantial and legally protectable interests—ranging from restitution as affected consumers to protections from ongoing retaliatory actions—cannot be adequately represented without their direct participation in these proceedings.

The motions are timely, and the Burkes have demonstrated the inadequacy of existing representation, the impairment of their interests without intervention, and the necessity of their involvement to ensure justice is served.

With these factors firmly established, the Burkes respectfully urge the Court to grant their motions, ensuring that justice is achieved and their rights are fully protected as intervenors.

RESPECTFULLY submitted this day, 25th of June, 2025

[1] 23STCV00341 – ANDREW LEHMAN, ET AL. VS MARK BURKE, ET AL, Los Angeles Superior Court, Judgment, Dec. 12, 2024.

[2] See; “Roadmap” Exhibit 222; Latest comment threats on LawsinTexas.com by Lehman, Exhibit 2222; Defendant & Proposed Intervenor’s Response & Plea To The Jurisdiction, 04/03/2025 in Harris County District Court Case # 202514896 – LEHMAN, ANDREW P vs. BLOGGER INC (Court 215).

[3] 23STCV00341 – ANDREW LEHMAN, ET AL. VS MARK BURKE, ET AL, Los Angeles Superior Court, “Case Type: Defamation (slander/libel) (General Jurisdiction), assigned to Judge Gail Killefer.

[4] 202514896 – LEHMAN, ANDREW P vs. BLOGGER INC (Court 215, NATHAN J. MILLIRON), Harris County District Court, Texas.

LITX

Jun 3 6, 2025

HOT OFF THE LIT PRESS #LITAMO2025

Lyin’ Lawyer Gabriel Hopkins of the CFPBCompare the response email today with the CFPB’s own website statement:

“Assuming continued available funds, the Bureau will work to provide full relief from this fund to eligible harmed consumers.” pic.twitter.com/lfA9mehhx6

— lawsinusa (@lawsinusa) June 6, 2025

Mr. Burke,

The action that CFPB filed against CFLA was a public regulatory action to enforce federal law.

It is not the proper forum for a private plaintiff to pursue individual claims for redress.

Redress for individual Affected Consumers was administered through a claims process overseen by the Bureau that is now closed.

As I noted in my previous response, the Bureau has concluded that you and Ms. Burke do not otherwise meet the standards for intervention as of right as articulated in the Ninth Circuit, including the element of timeliness.

As there does not appear to be any compromise position between intervention and non-intervention that the parties could pursue, we consider the obligation to meet and confer under Local Rule 7-3 to have been satisfied as to the Bureau.

Regards,

Gabriel Hopkins

Senior Litigation Counsel

Enforcement Division

Office: (202) 435-7842 | Mobile: (202) 714-4582

Consumer Financial Protection Bureau

consumerfinance.gov

LEHMAN’s $3M NEXT 🔥

California’s Dept of Financial Protection and Innovation said Wednesday that the CFBP is now making good on a $4.2 million redress plan for former students of a shuttered sales-training firm following agency delays and subsequent pressure from various states. pic.twitter.com/6uplRTZOyf— lawsinusa (@lawsinusa) June 5, 2025

Is the State of Texas helpin’ Felon on Paper n’ Pauper Andrew ‘Thug with a JD’ Lehman get clean for his divorce/custody case in Harris County District Court? Lots and lots of activity duly noted. pic.twitter.com/Hq3EevmmX9

— lawsinusa (@lawsinusa) June 4, 2025

Justice Comparison: Ex-Lawyer Burt ‘Maserati’ Burnett v. Andrew ‘Thug With a JD’ Lehman

Lawyer Burnett violates probation is jailed for 10 yrs. Convicted Felon Andrew Lehman Remains on Bond despite more violations than Burnett.https://t.co/rxur7W91h1 pic.twitter.com/0bvv2DoGgH

— lawsinusa (@lawsinusa) June 3, 2025

Bureau of Consumer Financial Protection v. Certified Forensic Loan Auditors, LLC

(2:19-cv-07722)

District Court, C.D. California

APR. 28

Good morning, Mr. Hopkins,

Thank you for your response.

After reviewing the details, I have a couple of questions regarding our recent phone conversation.

First, addressing the “Affected Consumer” element:

During our call, I informed you that Mr. Lehman explicitly admitted that Joanna Burke and John Burke qualify as “affected consumers” as defined in your stipulated judgment. Specifically, Paragraph 10 of the stipulated judgment states:

“A judgment for monetary relief is entered in favor of the Bureau and against Defendants CFLA and Lehman, jointly and severally, in the amount of $3 million for the purpose of providing redress to Affected Consumers.” (emphasis added)

Given this clear designation, what is your position on the refusal to grant an affected consumer access to financial redress? This is both a necessary and timely remedy.

Second, regarding the claim of “untimeliness”:

What is the intended purpose of a stipulated judgment that includes a five-year revocation period if there is no enforcement?

To illustrate, consider an analogy we discussed during our call: Mr. Lehman was revoked in Texas due to being in a stolen vehicle while in possession of, and under the influence of, a controlled substance—an incident that directly endangered his one-year-old child. This occurred alongside Ms. Monica Riley, who was also revoked and is now serving a five-year prison sentence.

Does a stipulated five-year civil judgment not function in the same manner?

For example, in CFPB v Prehired (adversary proceeding, Delaware Bankruptcy Court), there was also a stipulated final judgment issued in Case 23-50438-JTD, Doc 15, Filed 11/20/23.

I look forward to your clarification on these matters.

Sincerely

Mark Burke

Mr. Burke,

Thank you for the productive meet and confer conference on April 27. The Bureau does not consent to the proposed motion to reopen and intervene in Consumer Fin. Protection Bureau v. Certified Forensic Loan Auditors, LLC, et al., No. 19-07722, as the standards for intervention under Fed. R. Civ. Pro. 24 have not been satisfied.

The proposed intervention is untimely and unwarranted, as the CFPB’s regulatory enforcement action was resolved in 2020, and bears no legal relation to Andrew Lehman’s private state court action for defamation.

Any defenses to the claims in that action are properly presented in that forum, as appropriate.

To the extent you have concerns for your personal safety and that of your mother, we encourage you to contact local law enforcement to address them.

Sincerely,

Gabriel Hopkins

Good afternoon

Bureau of Consumer Financial Protection v. Certified Forensic Loan Auditors, LLC (2:19-cv-07722) District Court, C.D. California

Following our phone conversation on Tuesday 27 May 2025, I note that you were unable to provide an answer to the critical question: Are you opposed to the motion to reopen and intervene? I am now formally requesting an immediate response to this matter.

Additionally, I must bring to your attention the increasingly alarming threats issued by Texas felon on bond, Mr. Lehman, which now include vile and abusive attacks, particularly involving elder abuse. Given the severity of these communications, I have attached the most recent two emails for your review.

Your intervention is imperative to ensure the safety and integrity of those affected by this case, considering his history of violence, stalking, child end., and drug abuse. I expect a confirmation of receipt of this email and a direct update regarding both the motion to reopen and intervene as well as the steps CFPB will take regarding these threats.

This situation demands immediate action, and I trust that CFPB will prioritize its responsibility to address this urgent matter. I await your prompt reply.

Sincerely,

Mark Burke

What was meant to be a routine conference call regarding the Burkes’ Motion to Intervene unexpectedly transformed into a deposition of Mark Burke.

Despite Mark Burke’s transparency and open discussion, CFPB repeatedly deflected engagement—citing internal confidentiality, refusing comment, or vaguely promising to follow up without offering a deadline on this time-sensitive motion. When pressed for a commitment, the Bureau’s lawyers remained noncommittal, sidestepping the urgency of the matter.

Mark Burke firmly objected to the Bureau’s unwillingness to participate meaningfully in the conference. Instead of an open dialogue, the agency evaded substantive discussion, leaving critical questions unanswered.

Now, the decision rests with the Bureau: (i) stand by affected consumers in accordance with its mandate, or (ii) align itself—on paper—with an indicted felon out on bond.

Bookmark for updates.

Why is the motion to intevene filed again on May 13, 2025?

Answer, it’s a disguised ORDER Striking Pleading.

Email with court date stamped copy of motion to intervene and order.

National Treasury Employees Union v. Russell T. Vought

Court of Appeals for the D.C. Circuit

A federal appeals court panel on Monday blocked the Trump administration from moving forward with mass layoffs at the Consumer Financial Protection Bureau (CFPB), partially lifting a previous order construed as greenlighting the major cuts.

The panel on the U.S. Court of Appeals for the District of Columbia Circuit revoked its order allowing the administration to conduct reductions in force of employees if a “particularized assessment” determined their roles were unnecessary for the agency to perform its statutorily required duties.

The Trump administration took that previous order to mean it could move to lay off roughly 90 percent of CFPB’s staff, but a lower judge stepped in before the reduction occurred.

“Given these ongoing disputes, we think it best to restore the interim protection of paragraph (3) of the preliminary injunction, which ensures that plaintiffs can receive meaningful final relief should the defendants not prevail in this appeal, rather than continue collateral litigation over the meaning and reviewability of the ‘particularized assessment’ requirement imposed by this court’s stay order,” the panel wrote in an unsigned order.

Administration officials are set to appear before U.S. District Judge Amy Berman Jackson this week, as she considers whether the reduction in force violated her earlier order enjoining the administration from dismantling the agency.

The Trump administration was preparing to lay off more than 1,400 employees and revoke their computer access on April 18 before Jackson stepped in.

Officials contended that they were following the “particularized assessment” procedure laid out by the appeals court. The reduction would leave the CFPB with about 200 employees.

In the unsigned order, the judges newly defined “particularized assessment” as involving a determination that each division or office within CFPB can still perform its duties required by law without the employees being laid off. The determination must be made by the decisionmaker responsible for the reduction in force.

Despite that, they agreed to let the portion of Jackson’s injunction barring any major staff reductions to remain in effect while the appeal moves forward.

Judge Neomi Rao, an appointee of President Trump, wrote in a dissenting opinion that the panel’s decision barred leadership of the CFPB from abiding by Trump’s directive to cut back the agency.

“The district court overstepped our stay,” she wrote. “Rather than remedy the judicial error, today’s order hamstrings the Executive and prevents the CFPB from downsizing until the merits of the appeal are resolved.”

The judges wrote in the order that they already accommodated the government’s position by expediting its appeal, which is scheduled for oral arguments on May 16. There they will consider whether Jackson’s sweeping injunction stepped on the executive — but not before, they said.

The National Treasury Employees Union sued the administration in February, when acting CFPB Director Russell Vought took charge and ordered employees to halt all work. Jackson granted the union a preliminary injunction after the administration initially attempted to conduct mass layoffs.

SACRAMENTO – Today, Commissioner KC Mohseni of the Department of Financial Protection and Innovation (DFPI) and leaders from eleven states are pressing the federal Consumer Financial Protection Bureau (CFPB) to issue long-delayed restitution to victims of a predatory tech sales program.

In a letter sent today to the CFPB’s acting director, the multistate coalition details how a court order against Prehired, LLC and its related entities (Prehired) for illegal, deceptive, and abusive practices resulted in an award of $4.2 million in restitution to 660 consumers nationwide.

Unexplained delays at the agency level are keeping those checks from being distributed.

The court issued its order in November 2023 and the states worked with the CFPB to allocate funds for harmed consumers. The CFPB announced the allocation in May 2024.

States received regular updates throughout 2024 regarding the federal government’s progress to distribute these funds to Prehired’s victims.

In February of this year, the CFPB stopped providing information about the process.

Prehired misled consumers by promoting its vocational training program using deceptive claims.

It promised students a “6-figure sales career” within 12 months of completing the program and offered enrollment with “zero upfront costs” through income share agreements (ISAs).

These ISAs required students to repay a fixed percentage of their future income.

Prehired failed to disclose key terms, including that students would be required to pay even if they never secured a job.

In many cases, the company also raised minimum monthly payments without confirming whether students were employed or earning more.

These misrepresentations led many students to take on significant, unsustainable debt.

Once borrowers were indebted to Prehired, the company engaged in unfair debt collection practices by falsely representing the amount of debt owed by consumers and inducing students to enter into harmful “settlement agreements” that benefited Prehired.

The DFPI and various state attorneys general joined the CFPB in filing a complaint against Prehired under the Consumer Financial Protection Act of 2010 (CFPA) for its administration of ISAs used to finance students’ tuition.

The court found that Prehired’s conduct was unfair, deceptive, or otherwise unlawful and violated federal law. As a result, Prehired was ordered to repay $4.2 million in restitution to borrowers who entered into ISAs.

The letter urges the CFPB to provide a timeframe for when the agency plans to distribute the funds to victims.

The impacted consumers deserve the refunds that were secured for them.

Joining DFPI in the letter are Colorado, Delaware, Illinois, Massachusetts, Minnesota, New York, North Carolina, Ohio, Oregon, South Carolina, and Washington.

About DFPI

The Department of Financial Protection and Innovation protects consumers, regulates financial services, and fosters responsible innovation. DFPI protects consumers by establishing and enforcing financial regulations that promote transparency and accountability.

We empower all Californians to access a fair and equitable financial marketplace through education and preventing potential risks, fraud, and abuse.

Learn more at dfpi.ca.gov.

We are the Consumer Financial Protection Bureau (CFPB), a federal government agency that enforces laws that protect consumers. The CFPB and 11 state partners received a legal judgement against Prehired LLC, and other defendants.

On July 13, 2023, the Bureau and several state partners filed a complaint in an adversary proceeding against Prehired, LLC, Prehired Recruiting, LLC, and Prehired Accelerator, LLC. Prehired has its principal place of business in Delaware and, prior to filing bankruptcy, operated a private, for-profit vocational training program for software sales representatives. Prehired charged up to $30,000 for its program and encouraged consumers who could not pay upfront to enter into income share loans.

Prehired’s income share loans required consumers to make minimum payments equal to between 12.5% and 16% of their gross income for 4 to 8 years or until they had paid a total of $30,000, whichever was sooner.

Prehired transferred ownership of many of these loans to other entities, including Prehired Recruiting and Prehired Accelerator.

The complaint alleged that Prehired deceptively represented that its income share loans were not loans; deceptively represented that consumers would pay nothing until they had a job making at least $60,000 a year; and failed to disclose key financing terms required by the Truth in Lending Act (TILA) and Regulation Z.

The complaint also alleged that Prehired Recruiting engaged in unfair acts and practices by filing debt collection lawsuits in a distant forum when consumers neither lived in that forum nor were in that forum when they executed the financing agreement.

The complaint further alleged that Prehired Recruiting and Prehired Accelerator violated the Fair Debt Collection Practices Act (FDCPA) and the Consumer Financial Protection Act of 2010 (CFPA) by deceptively inducing consumers to enter into settlement agreements, and the FDCPA by claiming the consumers owed more than they did.

The attorneys general from Washington, Oregon, Delaware, Minnesota, Illinois, Wisconsin, Massachusetts, North Carolina, South Carolina, and Virginia, and California’s Department of Financial Protection and Innovation joined the action.

The Court signed the stipulated judgment and it became final on November 20, 2023.

The stipulated judgment orders consumer redress and a civil money penalty.

It also requires defendants to cease doing business and prohibits them from participating or assisting others in advertising, selling, or assisting in providing any consumer financial product or services relating to vocational education services.

The stipulated judgment also voids, and prohibits defendants from collecting on, Prehired’s income share loans or other consumer agreements that financed vocational education services.

Victim compensation

Payments have started in this case. The CFPB has contracted RUST Consulting to administer payments for this case and answer consumers’ questions. For questions related to this case, please:

Call: 1-888-516-0769

Email: prehired_info@rustcfpbconsumerprotection.org

Write: P.O. Box 2561, Faribault, MN 55021-9561

State of Washington – Consumer Protection Division v. Prehired, LLC (23-50438)

United States Bankruptcy Court, D. Delaware.

Consumer Financial Protection Bureau v. Portfolio Recovery Associates, LLC (2:23-cv-00110)

District Court, E.D. Virginia

Consumer Financial Protection Bureau (CFPB) v. Capital One, National Association (1:25-cv-00061)

District Court, E.D. Virginia

Consumer Financial Protection Bureau v. FirstCash Inc (4:21-cv-01251)

District Court, N.D. Texas

LITX

When the U.S. government supports criminality to silence dissent, the fight for truth becomes urgent.

THE BOOK OF LEHMAN exposes the depths of this ochlocracy. Read it now—take a stand for justice.

🔥 Stand for truth. Act now. https://t.co/hYg4qkbzpg pic.twitter.com/qqcgTmogIQ— lawsinusa (@lawsinusa) April 28, 2025

Bureau of Consumer Financial Protection v. Certified Forensic Loan Auditors, LLC

(2:19-cv-07722)

District Court, C.D. California

APR. 28

MARK BURKE AND JOANNA BURKE’S MOTION TO INTERVENE AND MOTION TO REOPEN CASE AS PLAINTIFFS AND MEMORANDUM OF LAW IN SUPPORT

Motion to Intervene

Proposed Intervenors, Mark Burke and Joanna Burke (“the Burkes”) contend that intervention is justified in this matter as their substantial interests are directly tied to the violations of the settlement of this litigation.

This motion is accompanied by the memorandum in support herein and follows Fed. R. Civ. P. 24(c). The Burkes highlight the relevance of the prior CFPB settlement with CFLA and Lehman, closed in July 2020, as it pertains to this motion. The Burkes contend that the settlement and related litigation significantly impact their interests and form the basis for this intervention.

Judicial Notice

The Burkes request judicial notice of the cited cases and references to establish their relevance to this matter. This request is made pursuant to the standards outlined in Dorsey v. Portfolio Equities Inc., 540 F.3d 333, 338 (5th Cir. 2008), and Lee v. City of Los Angeles, 250 F.3d 668, 688-89 (9th Cir. 2001).

Motion to Reopen Case

The Burkes respectfully request this court reopen this case. On June 20, 2020, there was an agreed settlement.

As part of this settlement, there was a STIPULATED FINAL JUDGMENT AND ORDER AS TO CERTIFIED FORENSIC LOAN AUDITORS, LLC (CA), CERTIFIED FORENSIC LOAN AUDITORS (TX) AND ANDREW P. LEHMAN, Dkt 93 (July 20, 2020).

Specifically, Paragraph 10 of the stipulated judgment states: –

“A judgment for monetary relief is entered in favor of the Bureau and against Defendants CFLA and Lehman, jointly and severally, in the amount of $3 million for the purpose of providing redress to Affected Consumers.” (emphasis added).

Background Summary

This Action

On July 20, 2020, the United States District Court for the Central District of California entered a final judgment resolving the Consumer Financial Protection Bureau’s (CFPB) allegations against Certified Forensic Loan Auditors, LLC (CFLA) and Andrew Lehman (Lehman). The CFPB alleged that CFLA and Lehman engaged in deceptive and abusive practices, including false claims about their services and qualifications, and charging illegal upfront fees, in violation of the Consumer Financial Protection Act of 2010 (CFPA) and Regulation O. The court permanently banned CFLA and Lehman from the industry, imposed a suspended $3 million restitution judgment, and levied a $40,000 civil penalty.

The Burkes qualify as Affected Consumers because Joanna Burke and her late husband, John Burke, were former clients of CFLA and victims of its deceptive practices according to Lehman, and as admitted in court proceedings. See; Judge Gail Killefer’s Default Judgment Opinion signed Dec. 2, 2024 at p.5, #3.[1]

Mark Burke has been directly impacted by Lehman’s unlawful actions, which surfaced after the settlement’s publication in July 2020, necessitating this intervention to reopen the case and secure restitution for these unresolved harms.

Lehman’s Civil and Criminal History Relevant to this Motion

Andrew Peter Lehman has a lengthy documented history of criminal actions and ongoing vexatious civil litigation, underscoring a pattern of misconduct.[2]

On January 9, 2023, Lehman initiated a defamation lawsuit in Los Angeles Superior Court (23STCV00341)[3] against Mark Burke and the republication of a CFPB article on LawsInTexas.com about the underlying case. Despite being domiciled in Texas and under criminal court supervision and bond restrictions, Lehman filed as a pauper and was granted In Forma Pauperis (“IFP”) status.

A void default judgment was later entered on December 12, 2024, awarding Lehman and co-Plaintiff Monica Lynn Riley, now incarcerated to serve out a five-year jail sentence, $1,991,194.12 in damages and injunctive relief. Lehman has since sought to domesticate this judgment in Harris County District Court (202514896)[4].

The Burkes Connection and Relevance

Joanna Burke and her late husband, John Burke, have faced prolonged litigation stemming from predatory mortgage lending practices. Notably, they prevailed in Deutsche Bank National Trust Company v. Burke, S.D. Texas, (4:11-cv-01658) and continue to address related issues, with Joanna currently engaged in active litigation against PHH Mortgage Corporation.

Mark Burke, on the other hand, operates Blogger Inc. and publishes investigative journalism through LawsInTexas.com. His connection to the case arises from Lehman’s legal actions targeting his publication and the article regarding the CFPB settlement.

Lehman’s actions, directly affect the Burkes interests and underscore their need to intervene in the CFPB settlement case.

Memorandum of Law in Support of Intervention

Mark Burke is the proprietor of Blogger Inc., a nonprofit entity registered in Delaware and the legal blog LawsinTexas.com, which is dedicated to investigative journalism, particularly focusing on legal matters of public concern. To comprehend the significance, a brief overview is necessary. Behind every business stands an owner, entwined with a personal life. In Mark’s case, his digital media businesses facilitate a home office, doubling as his residence, which has been embroiled in prolonged litigation due to a predatory loan, which became the focus of a federal lawsuit, Deutsche Bank National Trust Company v. Burke (4:11-cv-01658) District Court, S.D. Texas, commenced Apr. 11, 2011. Legally owned by Joanna Burke, Mark’s mother, the property has hosted Mark’s home office since 2009.

John and Joanna Burke defeated Deutsche Bank twice in the 2011 proceedings, first at a bench trial in 2015 and again on remand in late December of 2017. However, Joanna Burke is still embroiled in an active civil suit against PHH Mortgage Corporation in Burke v. PHH Mortgage Corporation which relates to the 2011 proceedings.

At all times, the home remains the permanent residence of the Burkes.

Intervention Under Civil Rule 24(a)(2)

Under the Federal Rules of Civil Procedure, Proposed Intervenor must satisfy four essential requirements for intervention: timeliness, a necessary interest, impairment of that interest without intervention, and the inadequacy of protection absent intervention (Fed. R. Civ. P. 24(a)(2)).

Necessary Interest

As explained above, the Proposed Intervenors have asserted their direct interest in the subject matter of the litigation, a necessary condition for intervention (Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001)).

This interest, related to the subject of the action, is legally protectable even if not enforceable, as per Wal–Mart Stores, Inc. v. Tex. Alcoholic Beverage Comm’n, 834 F.3d 562, 566 (5th Cir. 2016). Joanna Burke’s interests are as an “affected consumer” who has been subjected to stalking, as well as vile and harassing behavior by Lehman. He has made derogatory statements and has stalked her home while under strict supervision of Texas courts (wearing an ankle monitor). He and left repulsive statements on the front of documents left on her front door and created a website slandering her name and reputation and that of her deceased husband. These are detailed in related proceedings, listed herein, including Case No. 202311266 – KRUCKEMEYER, ROBERT J vs. BLOGGER INC D/B/A LAWIN TEXAS.COM (Court 152), Harris County District Court, Texas, Addendum L, Img # 108883355, 06/27/2023.

Mark Burke is intricately tied to Lehman due to his ongoing vexatious litigation targeting Mark Burke and his business interests. The imminent threat to his home office (residence) as a result of the latest legal maneuver by Lehman directly implicates his business, possessions, civil liberty, and constitutional rights.

As a result, the urgency of the Burke’s proposed intervention is evident in the intertwined personal, business, and legal battles. It is necessary that the Burkes obtain intervention in these proceedings as interested parties and affected consumer(s).

Timeliness of Intervention

This motion to intervene is timely, in alignment with the contextual nature of the timeliness inquiry (Sierra Club v. Espy, 18 F.3d 1202, 1205 (5th Cir. 1994)); California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006). This case involves a 5-year period tied to the deferred penalties, and the Burkes have filed this motion before that period expires. Their filing also follows Lehman’s attempt to domesticate a void judgment of nearly $2 million and his threats to foreclose on the Burkes residence, further emphasizing the urgency of their intervention.

Moreover, recent developments lend further weight to this motion. Following political changes after the 2024 election and the CFPB’s deactivation, enforcement efforts were significantly delayed or discontinued. Despite these challenges, the Ninth Circuit’s recent ruling in Consumer Financial Protection Bureau v. CashCall, Inc., No. 23-55259 (9th Cir. Apr. 24, 2025) confirms that judgments from prior CFPB actions remain enforceable, including restitution.

Impairment of Interest Without Intervention

Without intervention, the Burkes substantial interests — including their rights to restitution and protection from further harm — would be significantly impaired.

Joanna Burke, a former client of CFLA and victim of Lehman’s deceptive practices, has a direct stake in the restitution outlined in the CFPB settlement.

Mark Burke faces ongoing litigation and direct challenges to his investigative journalism as a result of Lehman’s retaliatory actions, further underscoring the need to safeguard their rights. Adequate representation is lacking due to the CFPB’s current standing with the present administration, necessitating intervention to ensure their interests are preserved.

Intervention is crucial to safeguard these interests, as recognized in cases such as Atlantis Dev. Corp. v. United States, 379 F.2d 818, 828-29 (5th Cir. 1967). The Fifth Circuit has established that intervention is warranted when significant interests may be impaired without direct representation. Similarly, the Ninth Circuit in California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006), emphasized that intervention is appropriate where a party demonstrates a substantial interest that risks being impeded or impaired if intervention is denied, particularly when existing parties cannot adequately represent that interest.

The Burkes rights to restitution and protection from Lehman’s actions align with these principles, underscoring the necessity of intervention to ensure their interests are preserved.

Inadequacy of Protection Absent Intervention

The Burkes assert that their interests cannot be adequately protected without intervention. The CFPB, while instrumental in the original settlement, has demonstrated a lack of action in responding to the Burkes requests for assistance.

Relying on the CFPB’s 2020 settlement with CFLA and Lehman, the Burkes sought Lehman’s current address to address ongoing harassment and retaliatory actions against them. Despite detailing the harm caused by Lehman, including stalking, slander, vexatious litigation, and threats to their residence, the CFPB arranged a phone call with Mark Burke, but during this phone call declined to act on their behalf or provide a current address for Lehman, which had been requested to address these ongoing retaliatory actions.

This refusal emphasizes the CFPB’s inability to enforce the settlement terms, including securing restitution for affected consumers as outlined in the $3 million judgment.

Mark Burke seeks intervention to ensure proper restitution and protect his financial interests. Lehman’s ongoing legal maneuvers — such as his efforts to domesticate a void $2 million judgment through litigation — further highlight the urgency of intervention to safeguard the Burkes rights.

These retaliatory actions directly impact the Burkes property, personal safety, financial well-being, and constitutional rights, necessitating representation beyond what the CFPB can offer.

Judicial precedents strongly support intervention under circumstances where existing parties fail to adequately protect substantial interests.

As established in Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001), intervention ensures that legally protectable interests are represented effectively.

Similarly, California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006) underscores that intervention is warranted when a party’s interests risk being impaired without direct involvement.

The Burkes unique position as affected consumers and subjects of Lehman’s retaliatory actions further demonstrate the inadequacy of protection absent their intervention.

Declaration

Pursuant to 28 U.S.C. § 1746, a litigant may submit an unsworn declaration in lieu of a sworn affidavit as evidence in federal court proceedings, including in opposition to summary judgment. See Nissho-Iwai Am. Corp. v. Kline, 845 F.2d 1300, 1305 (5th Cir. 1988) (‘Section 1746 allows a written unsworn declaration, subscribed as true under penalty of perjury, to substitute for an affidavit.’).

This principle has also been upheld in the Ninth Circuit. See Schwarzer, Tashima & Wagstaffe, Federal Civil Procedure Before Trial, § 14:131 (The Rutter Group 2025) (‘Unsworn declarations under penalty of perjury are permissible under 28 U.S.C. § 1746 and carry the same evidentiary weight as affidavits.’).

I, Mark Stephen Burke, my date of birth is June 20, 1967, residing at 46 Kingwood Greens Dr, Kingwood, Texas, 77339, declare under penalty of perjury under the laws of the United States of America that the information contained herein is true and correct.

I, Joanna Burke, my date of birth is November 25, 1938, residing at 46 Kingwood Greens Dr, Kingwood, Texas, 77339, declare under penalty of perjury under the laws of the United States of America that the information contained herein is true and correct.

Conclusion

For the foregoing reasons, the Burkes respectfully request that this Court grant their (i) motion to reopen the case and (ii) motion to intervene.

The Burkes meet all the legal requirements for intervention as established by relevant judicial precedents, including Ford v. City of Huntsville, 242 F.3d 235, 240 (5th Cir. 2001), and California ex rel. Lockyer v. United States, 450 F.3d 436, 441 (9th Cir. 2006).

Their substantial and legally protectable interests—ranging from restitution as affected consumers to protections from ongoing retaliatory actions—cannot be adequately represented without their direct participation in these proceedings.

The motions are timely, and the Burkes have demonstrated the inadequacy of existing representation, the impairment of their interests without intervention, and the necessity of their involvement to ensure justice is served.

With these factors firmly established, the Burkes respectfully urge the Court to grant their motions, ensuring that justice is achieved and their rights are fully protected as intervenors.

RESPECTFULLY submitted this day, 28th of April, 2025

4/28/2025 at 4.06 pm.

This email confirms that the document(s) listed below were received by the United States District Court for the Central District of California at the date and time indicated:

Name: Mark Burke

Tracking Number: EDS-250428-001-9659

Date: 4/28/2025 2:05:44 PM

Uploaded files:

2024_MBurke_and_JBurke_Intervenors_CFPB_Lehman_PropOrder_Apr28_2025.pdf

Proposed Order

2024_MBurke_and_JBurke_Intervenors_CFPB_Lehman_Apr28_2025_Final.pdf

Motion to Intervene

The document(s) have not yet been filed. Just like documents received through the U.S. Mail, documents received through the Electronic Document Submission System (“EDSS”) will not be considered filed until court staff have uploaded them into the Court’s Case Management/Electronic Case Filing System (“CM/ECF”). Documents submitted using EDSS will be processed in the order they are received and should be uploaded to CM/ECF within 3-5 business (or court) days after receipt. However, the date of EDSS submission will be considered the filing date for any documents received through EDSS and later filed into CM/ECF.

If you are registered for electronic service of documents and receiving e-service in this case, you will receive a Notice of Electronic Filing (“NEF”) from the CM/ECF System as soon as each document listed above has been filed. (Click here for information about registering for electronic service or to add e-service in this case.) If you are not registered for electronic service, you may check the status of your documents by checking the docket for your case on PACER (https://pacer.uscourts.gov). Please wait at least two business days after receiving this email and check the docket for your case on PACER before contacting the Court regarding the status of documents submitted through EDSS.

If you are trying to file a document in a case pending before the United States Bankruptcy Court, or in any case pending in any court other than the United States District Court for the Central District of California, your document will not be filed and you will not receive any response to your EDSS submission. Likewise, if you are an attorney required by the local rules to file your documents electronically using the Court’s CM/ECF System, your document(s) will not be filed if submitted through EDSS, and you will not receive any further communication from the Court about your EDSS submission.

Please include the tracking number listed above as your reference on any communications with the Court about this submission. We recommend that you keep this email for your records.

Civil Intake

United States District Court

Central District of California

Tel: (213) 894-3535

HCD COURT #215

TRCP 145 (d)

Defects: The clerk may refuse to file a Statement [of Inability to Pay Costs] that is not sworn to before a notary or made under penalty of perjury.

Felon on Paper Andrew Lehman filed an unsigned application of indigency for Incarcerated Monica Riley. pic.twitter.com/bMT6ijuHWC— lawsinusa (@lawsinusa) April 26, 2025

Consumer Financial Protection Bureau Announces Settlement with Foreclosure Relief Services Company and Its Owner

WASHINGTON, D.C. – On July 20, 2020, the United States District Court for the Central District of California entered a stipulated final judgment resolving the Consumer Financial Protection Bureau’s (Bureau) allegations against Certified Forensic Loan Auditors, LLC (CFLA) and Andrew Lehman (Lehman). CFLA is a foreclosure relief services company headquartered near Houston, Texas, and Lehman is CFLA’s president and CEO. The Bureau alleged that CFLA and Lehman engaged in deceptive and abusive acts or practices in violation of the Consumer Financial Protection Act of 2010 (CFPA) and charged unlawful advance fees in connection with marketing and selling financial advisory and mortgage assistance relief services to consumers in violation of Regulation O and the CFPA. The court’s order permanently bans CFLA and Lehman from the industry and imposes a suspended judgment for redress of $3 million and civil money penalties of $40,000.

The Bureau’s complaint, which was filed on September 6, 2019, and amended on November 13, 2019, alleged that CFLA and Lehman made deceptive and unsubstantiated representations about the company’s mortgage assistance relief services and its ability to help consumers avoid foreclosures or negotiate loan modifications. Specifically, the amended complaint alleged that the company made deceptive and unsubstantiated claims about the efficacy and content of its services, as well as false claims about the experience and qualifications of the people performing those services. The Bureau also alleged that the company’s conduct constituted abusive acts or practices in violation of the CFPA. Finally, the Bureau alleged that CFLA and Lehman charged consumers illegal upfront fees in violation of Regulation O, which governs the offering or provision of mortgage assistance relief services.

The court’s order permanently bans CFLA and Lehman from providing mortgage assistance relief services or financial advisory services. The order also imposes a suspended judgment against CFLA and Lehman for redress of $3 million and imposes a civil money penalty of $40,000. The suspended judgment for redress and the amount of the civil money penalty account for CFLA’s and Lehman’s limited ability to pay based on sworn financial statements. Whenever the Bureau collects a civil money penalty through an enforcement action, that penalty is deposited into the Bureau’s Civil Penalty Fund. Assuming continued available funds, the Bureau will work to provide full relief from this fund to eligible harmed consumers.

CFLA and Lehman were the only remaining defendants in the Bureau’s lawsuit. The court previously entered a final judgment resolving the Bureau’s allegations against Michael Carrigan, CFLA’s former auditor.

The stipulated final judgment and order against Carrigan is available at: https://files.consumerfinance.gov/f/documents/cfpb_CFLA-lehman-carrigan_final-stipulated-judgment-order_2019-10.pdf

The amended complaint is available at: https://files.consumerfinance.gov/f/documents/cfpb_cfla-lehman-carrigan_amended-complaint_2020-07.pdf The stipulated final judgment and order against CFLA and Lehman is available at: https://files.consumerfinance.gov/f/documents/cfpb_cfla-lehman-carrigan_final-stipulated-judgment-order_2020-07.pdf.pdf

Auto Mogul Ashworth Barnes Faces Billion Dollar Debt Recall as Bandit Bob Takes Frosty’s 713 Call

Houston’s Auto Tycoon Ashworth Barnes on a Collision Course as Frost Bank’s $1B+ Debt Recall Hits, with Bob Kruckemeyer Answering the 713 Call

Magistrate Judge Bill Davis Offers Two Contrasting Reports by Applying Void-Judgment Exception

US Bank avoids dismissal under Rooker–Feldman. It has carried its burden to show that its suit falls within the void-judgment exception.

Texas Supreme Court: Don’t Take a Man at His Word as Verbal Agreements are Worthless

Fraud by non-disclosure arises only when the defendant, among other things, has a legal duty to disclose facts to the plaintiff.

{kind=link}

{kind=link}

{kind=link}

{kind=link}