UPDATE; Nov. 10, 2019; Six Ex-Deutsche Bankers Jailed along with Nomura Bankers for Paschi Roles

Italy took a hard line against bankers involved in helping Banca Monte dei Paschi di Siena SpA falsify its accounts, sentencing 13 executives and managers to jail terms and fining the banks that worked with the Italian lender.

Monte Paschi ex-Chairman Giuseppe Mussari was sentenced to 7.6 years in prison.

Deutsche Bank officials Michele Faissola and Michele Foresti and Nomura’s Sadeq Sayeed, Raffaele Ricci also received jail terms. Deutsche Bank and Nomura face fines and seizures totaling about 160 million euros ($176 million) for their roles.

Monte Paschi’s managers were accused of colluding with Deutsche Bank and Nomura bankers to hide losses at the Italian lender by using complex derivatives trades, dubbed Santorini and Alexandria, that led to a misrepresentation of its finances between 2008 and 2012. Paschi reached a plea-bargain deal in 2016 in one of the highest profile European banking cases in the last decade, first revealed by Bloomberg News.

A spokesman for Monte Paschi declined to comment.

All of the 13 suspects from the three banks received prison terms, including Antonio Vigni, Monte Paschi’s former general manager and ex-CFO Daniele Pirondini. The court convicted two of the group of managers despite the prosecution calling for their acquittal.

Prosecutors argued that the complex transaction Deutsche Bank helped put in place in 2008 hid about 430 million euros of losses that Paschi was facing on a previous deal, while Nomura’s derivative hid more than 300 million euros of losses not reported in the bank’s 2009 income statement.

Both transactions were carried out to cancel previous losses by building up two-leg deals, with one leg granting Monte Paschi an immediate gain and the other loss-making one designed to last for several years in order to pay back the investment banks for the gains realized by Paschi on the first one, according to prosecutors.

The judge also requested the prosecutor to look into some of the witnesses who testified during the trial, including former Deutsche Bank official Stefano Dova.

Shocked, Disappointed

Giuseppe Iannaccone, the lawyer defending former Deutsche Bank executives in Monte Paschi case, said in statement he’s “shocked” by the ruling and fully convinced of his clients’ innocence.

“We are disappointed with the verdict,” Frankfurt-based Deutsche Bank said in a statement. “We will review the rationale for it once it is published.”

Deutsche Bank defendants in previous hearings had rejected the allegations of a deliberate effort to hide losses, saying that Santorini was a legitimate deal and carried risk, and was not designed as a sure-fire bet.

Nomura “is disappointed with the verdict,” it said in a e-mailed statement. “After thoroughly examining the content of the judgment, the company will consider all options, including an appeal.”

Nomura’s lawyers during the trial also argued that the Alexandria deal was legitimate and an attempt to mask losses. Monte Paschi’s lawyers also rejected the allegations against their defendants, arguing that the deals were conceived to boost Monte Paschi’s interest margin and reduce previous risks.

Undermined by souring loans and derivatives deals that backfired, Monte Paschi requested state aid in 2017. The Italian government stepped in to take a stake of about 68 percent, injecting 5.4 billion euros in aid as part of an 8.3 billion-euro recapitalization.

Defendants convicted and their roles at the time of the transactions

Six Former Deutsche Bank Executives Jailed:

Michele Faissola, head of global rates: 4.8 years

Michele Foresti, head of structured trading: 4.8 years

Dario Schiraldi, head of European sales: 3.6 years

Marco Veroni, account manager: 3.6 years

Ivan Dunbar, co-head of global capital markets: 4.8 years

Matteo Vaghi, head of Italian sales: 3.6 years

Ex-Nomura

Sadeq Sayeed, CEO of Nomura Europe subsidiary: 4.8 years

Raffaele Ricci, head of sales for Europe, Middle East: 3.5 years

Ex-Paschi

Giuseppe Mussari, Chairman: 7.6 years

Antonio Vigni, General Manager 7.3 years

Daniele Pirondini, CFO: 5.3 years

Gianluca Baldassarri, head of finance division: 4.8 years

Marco Di Santo, head of asset liabilities management division: 3.6 years

As Six Former Deutsche Bankers Are Convicted in Italy, We Look Back at the Deutsche Bankers that Never Testified, Because they Died in Suspicious Circumstances

How Deutsche Bank Made a $462 Million Loss Disappear

A dubious trade leads to a criminal trial for Europe’s most important bank.

On Dec. 1, 2008, most of the world’s banks were still panicking through the financial crisis. Lehman Brothers had collapsed. Merrill Lynch had been sold. Citigroup and others had required multibillion-dollar bailouts to survive. But not every institution appeared to be in free fall. That afternoon, at the London outpost of Deutsche Bank, the stolid-seeming, €2 trillion German powerhouse, a group of financiers met to consider a proposal from a team led by a trim, 40-year-old banker named Michele Faissola.

The scion of an Italian banking family, Faissola was the head of Deutsche’s global rates unit, a division that created and sold financial instruments tied to interest rates. He’d been studying the problems of one of Deutsche’s clients, Italy’s Banca Monte dei Paschi di Siena, which, as the crisis raged, was down €367 million ($462 million at the time) on a single investment.

Losing that much money was bad; having to include it in the bank’s yearend report to the public, as required by Italian law, was arguably much worse.

Monte dei Paschi was the world’s oldest bank. It had been operating since 1472, not long after the invention of the printing press, when the Black Death was still a living memory.

If investors were to find out the extent of its losses in the 2008 credit crisis, the consequences would be unpredictable and grave: a run on the bank, a government takeover, or worse. At the Deutsche meeting, Faissola’s team said it had come up with a miraculous solution: a new trade that would make Paschi’s loss disappear.

The bankers in the room had seen some financial sleight of hand in their day, but the maneuver that Faissola’s staffers proposed was audacious. They described a simple trade in two parts. For one half of the deal, Paschi would make a sure-thing, moneymaking bet with Deutsche Bank and use those winnings to extinguish its 2008 trading losses.

Of course, Deutsche doesn’t give away money for free, so for the second half of the deal, the Italians would make a bet that was sure to lose.

But while the first transaction was immediate, the second would play out slowly, over many years. No sign of the €367 million sinkhole would need to show up when Paschi compiled its yearend financial reports.

The audience for the proposal that day was Deutsche’s global market risks assessment committee, a top-level panel that reviews transactions with legal, regulatory, and reputational considerations. Respectively, that means asking: Is a given trade within the law? Is it within the looser framework of industry rules and standards? And even if so, can Deutsche pull it off without maiming its brand—its basic ability to operate as a trustworthy member of the global financial system?

To at least one member of the committee, the possibilities of Faissola’s trade seemed wondrous. “This is fantastic,” said Jeremy Bailey, Deutsche’s European chairman of global banking, according to testimony of an executive who later recounted the exchange for an internal disciplinary panel. “You can book a [profit] in front and spread losses over time?” Bailey added. “We should do it for Deutsche Bank.”

Ivor Dunbar, the meeting’s chairman, curbed Bailey’s enthusiasm. “We are not discussing [our] balance sheet here,” he said. (Bailey, through a spokesman, denies he made the remarks.)

Outside the room, one of Faissola’s longtime colleagues was raising questions about the deal. William Broeksmit, a managing director who specialized in risk optimization, was concerned about the winner-loser construction.

A Chicago-born son of a United Church of Christ minister, Broeksmit had decades earlier been a pioneer in interest rate swaps, the financial instruments that had rewritten the possibilities—and profitability—of investment banking.

But Broeksmit, 53, was also against reckless derivative deals, which is how he viewed Faissola’s proposal, according to a person familiar with his thinking. Eleven minutes after the meeting began, Broeksmit e-mailed one of its attendees with a warning about the Paschi trade and its “reputational risks.”

The message had no effect. When the meeting ended after almost 90 minutes, Faissola got a go-ahead—setting in motion a scandal that has resulted in a criminal trial now under way in Milan.

A judge there has accused Deutsche Bank and five former executives, including Faissola and Dunbar, of colluding with Paschi to falsify its accounts in 2008. (None of Deutsche’s top managers at the time has been accused of wrongdoing. Faissola declined to comment for this article, as did both banks. Dunbar didn’t respond to requests for comment.)

Eight years after the financial crisis, the stakes could hardly be higher. Being the biggest bank in Germany makes Deutsche the most important bank in Europe, and the Paschi trial is an uncomfortable reminder that its operations, already with barely enough capital to meet industry standards, are threatened by persistent scandal. Deutsche is also facing investigations into whether it helped clients launder billions out of Russia.

This month the bank agreed to pay $7.2 billion to resolve a U.S. probe into its subprime mortgage business, admitting it misled investors. [But Deutsche Bank decided to cancel the deal, without any objection by the U.S.]. Deutsche has paid more than $9 billion in further fines and settlements related to claims of tax evasion; violating sanctions against Iran, Libya, Syria, Myanmar, and Sudan; rigging the $300 trillion Libor market; and other alleged breaches of the law.

The strain has intensified concerns about Deutsche’s balance sheet, which contains one of the world’s largest pots of most-difficult-to-quantify risk. The bank says it’s trimmed some of its exposure, as John Cryan, who became chief executive officer in 2015, attempts to clean up his predecessors’ messes.

But if Deutsche ever requires government help, such as a bailout, the effects could be catastrophic for more than shareholders. In recent years, as the euro community has faced one solvency problem after another in Greece, Portugal, and elsewhere, Germany’s Angela Merkel has been chief scold. She’s insisted on fiscal pain for irresponsible actors and pushed for banking rules that keep taxpayers from picking up the bills again for reckless financiers. Her government coming to the aid of Deutsche Bank after lecturing others on restraint would be the ultimate euro zone irony.

In a worst-case scenario, it could trigger a furor that finally brings down the continent’s currency, already made fragile by Brexit, refugees, and the rise of nationalist politicians.

The bank’s deal with Paschi is a microcosm of how Deutsche’s embrace of derivatives, questionable accounting, and slow-walking of regulators have eroded the market’s trust to the point that no one really knows how close the company is to the edge. What exactly happened in the days surrounding the December 2008 meeting in London is key to the Italian prosecution.

The German financial-markets regulator, known as BaFin, already tried to get to the bottom of the matter, commissioning an independent audit in January 2014.

The ensuing report has never been made public, but Bloomberg Businessweek obtained a copy. It shows that auditors asked Faissola what happened that afternoon in London. Other participants recalled details and dialogue, the report says, but Faissola drew a blank about the event he’d helped run. Broeksmit wasn’t interviewed. On Jan. 26, 2014, the day before the audit began, his body was found at his London home, hanging from a dog leash.

Founded in 1870, Deutsche Bank was for most of its existence content to take deposits and make loans; in the 1920s it participated in the founding of the airline Lufthansa and the merger of automakers Daimler and Benz.

Then, in the 1980s and ’90s, Deutsche watched as rival lenders in London and across the U.S. turbocharged profit growth by snapping up boutique investment banks and hiring or building teams to sell higher-margin financial products.

To join the bonanza, Deutsche in 1995 hired one of its leaders from Merrill Lynch: Edson Mitchell, a redheaded chain smoker from Maine who was nurturing a team of future financial leaders.

His crew included Broeksmit, the swaps innovator, and Anshu Jain, a prodigy at selling such risky, fee-laden products to hedge funds. Three years later, Deutsche made an even more emphatic attempt to buy its way into investment banking’s culture and profits, acquiring Bankers Trust—a New York derivatives house notorious for its cowboy culture—for about $10 billion.

If longtime Wall Streeters gawked at first at the German interloper, they quickly recognized that Deutsche had adopted their aggression and then some: Mitchell and his deputies expanded Deutsche’s London-based investment banking operation until it made half the bank’s revenue by the turn of the century.

Mitchell didn’t live to see Deutsche complete its transformation into a financial omnivore. Three days before Christmas 2000, he was riding in a small Beechcraft Super King Air 200 plane along the coast of Maine toward his vacation home in Rangeley. The wreckage was found the next morning, not far from the summit of Beaver Mountain. He was 47.

Afterward, Jain took over as head of global markets. One of his deputies was Faissola.

Faissola represented the next generation in Deutsche’s investment banking push. He was born in 1968 in Sanremo, the coastal town whose legendary song contest launched the tune Volare, and his uncle was president of the Italian banking association.

While running Deutsche’s global rates division in London for Jain, Faissola built his own fortune, at times earning tens of millions of pounds a year. He drew the jealousy of British co-workers because, as a foreigner, he was able to legally avoid U.K. tax on his bonuses. Faissola’s town house in Chelsea featured an indoor pool.

In the first years of the millennium, Deutsche bankers chased new sources of riches around the globe. People who piled into uncharted areas or pushed the rules were rewarded handsomely. Starting in 2005, Deutsche traders in Europe, North America, and Asia manipulated a benchmark interest rate to benefit their own derivative bets, according to an indictment made public last year in federal court in New York City.

Deutsche’s most profitable derivatives trader earned a bonus of almost £90 million (then $130 million) in 2008 alone.

Deutsche bankers also increased their bonuses in the runup to the crisis by creating and selling to clients mortgage securities that were marketed as high-quality investments but were in fact loaded with home loans destined to go bust. For clients, Deutsche became a go-to bank when they wanted risk and complexity.

In May 2002, when it was 530 years old, Monte dei Paschi asked Deutsche Bank to sell it something complicated. Paschi had recently listed its shares on the Italian stock exchange and was under pressure to grow. It owned a piece of another bank known today as Intesa Sanpaolo and wanted to convert some of that stake into cash for acquisitions, while still benefiting from any rise in Intesa’s shares—a kind of have-cake-and-eat-it-too arrangement.

It was exactly the kind of bespoke financial product the new, risk-friendly Deutsche was growing fat on.

The two banks created a venture called Santorini Investments—essentially, a derivative bet in the form of a company. The bet would pay off if Intesa shares rose and would lose value if they fell. Later restructuring made Paschi the sole shareholder.

The switch meant that in 2008, when bank stocks tanked in the worldwide financial crisis, Paschi took all of the losses, which swelled from €180 million in early October to more than €300 million in the following weeks.

The bank’s own shares were on their way to losing half their value since the start of the year. If Paschi included the Santorini loss in its Dec. 31 reports, the consequences would be dire: Italy’s central bank could take over its administration or force a bailout that would wrest control from its owners, a politically connected Siena foundation.

As the losses grew, Deutsche executives knew time was running out for Paschi to find a solution.

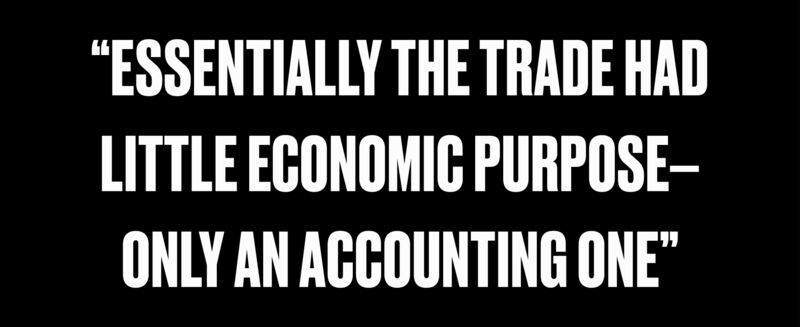

Having done the first deal, they went to Paschi management with a proposal for a second that would both help the Tuscan bank and be a new source of fees for Faissola’s group. On Nov. 3 they sent Paschi draft contracts for the sure-to-win/sure-to-lose trade that straddled the new year. Each prong of the bet simply wagered on an index that was the exact inverse of the other. Essentially, the trade had little economic purpose—only an accounting one.

That’s typically a red flag to auditors and regulators, and it took almost a month for Deutsche to alter the deal so it contained a small amount of actual risk. The bankers did this by mixing in two interest rate triggers—that is, prices to be fed into a formula that would determine how much money the participants in the trade had to pay or receive from each other.

But that created a slight possibility that Paschi could win both sides of the bet. To mitigate this potential Deutsche loss—as much as €500 million—Deutsche added a third trigger. Underlying the now complex flowcharts of rates, payments, and triggering events was the asset on which the transactions were to be based: about €2 billion in Italian government bonds.

Further illustrating the incestuousness of the deal, Paschi would need to buy the bonds and hand them over to Deutsche as collateral. Deutsche, for the sake of its own accounting, would need to sell the bonds to come up with cash that it then would give right back to Paschi to pay off the Santorini loss. And Paschi would buy the bonds in the first place from a third bank that had bought them from Deutsche.

By Dec. 1, 2008, Faissola’s group was ready to present the deal to Deutsche’s risks assessment committee, which sent it along to a final bureaucratic stage: the market risk management approval committee, where Broeksmit had influence.

Top management had just handed Broeksmit broad authority to police risk across the firm, rehiring him after he’d taken a hiatus as a consultant. Michele Foresti, a managing director who reported to Faissola, e-mailed Broeksmit on Dec. 2, copying his boss.

“I understand market risk management doesn’t want to give us green light to close this transaction,” Foresti wrote, noting the small chance of a €500 million loss. “I feel the risks are important but we should be able to manage them, could we sit down to discuss as soon as you have 5 mins?” Broeksmit’s reply was terse: “I think this should be presented to Anshu.”

Anshu Jain was by then co-head of investment banking at Deutsche.

Foresti sent another e-mail at 3:52 p.m. the next day: “still waiting for [committee] approval, faissola is in anshu’s office.” What, if anything, Jain knew about the deal was an avenue later explored in the German regulator BaFin’s audit. It found no evidence to suggest Jain was aware of the transaction and couldn’t conclude whether he’d been involved in its approval.

Jain told the inquiry that he wasn’t part of that process, though he couldn’t rule out having heard about the Paschi transaction in a general meeting. Faissola said he couldn’t recall having talked with Jain about the transaction. Faissola could have been in Jain’s office for many reasons. (Jain declined to comment for this article. Foresti, who’s a defendant in the Milan case, also declined to comment.)

Deutsche’s risk committee signed off on the Santorini project by the end of the day, after first securing a concession that Paschi would sign a memo pledging to inform its own auditors about the deal and consult its own legal and accounting advisers. The two parties executed the first part of the trade that night by phone, and the rest of the paperwork was signed over the following two days.

The deal allowed Paschi an immediate gain of €364.1 million, neutralizing the derivative loss. Deutsche netted about €60 million in fees, according to documents seen by Bloomberg Businessweek. Internally, the profits were credited to Faissola’s unit.

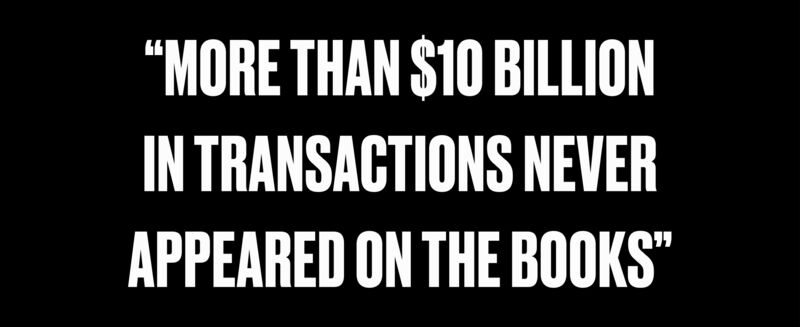

Deutsche also benefited from the way it accounted internally for its side of the deal. That complex shuttling of Italian bonds? The bank decided that all of the back-and-forth maneuvers canceled themselves out and did not need to appear on its balance sheet.

Deutsche began to apply the practice to transactions around the world, totaling more than $10 billion that never showed up on its books and making the bank look smaller and less risky than it really was.

In September 2009, it was Broeksmit again who took notice. In an e-mail about a similar deal, he wrote that such accounting techniques “may be a rounding error at this point, but [they are] growing quickly.”

An anonymous whistle-blower contacted Italian authorities and the U.S. Federal Reserve about Santorini, and they started parallel probes in 2011. In the fourth quarter of that year, Deutsche appeared to resist the Fed’s questions, and likely because of the delays and insufficient replies—according to the BaFin audit—the Fed issued a subpoena in April 2012.

Jain was promoted to co-CEO the next month. He proposed Broeksmit as the new chief risk officer, but had to back off after BaFin objected, noting that he’d never managed a large number of employees. Broeksmit retired in February 2013—out of the bank, but well aware of the mounting investigations into the Deutsche-Paschi deal. In subsequent months he complained to a psychiatrist that he was suffering from anxiety about being investigated.

At the same time, Santorini exploded in Italy as a national scandal. In January 2013, Bloomberg News reported that Paschi executives had used the deal to improperly obscure losses—provoking criminal investigations, tanking the bank’s stock, and, in February 2013, leading to a government bailout of €4.07 billion.

Among the casualties was David Rossi, Paschi’s communications chief. At about 9 p.m. on March 6, a bank employee noticed that Rossi was missing from his fourth-floor office. A window had been left open.

Authorities found Rossi’s body in a courtyard below. Rossi, 51, wasn’t himself the subject of any inquiries, but his home had been searched two weeks earlier by police. His death was at first ruled a suicide, but the inquest has been reopened based on evidence his wife presented, including security video that shows Rossi fell out backward.

Several months after Rossi’s death, in January 2014, Broeksmit was supposed to meet his wife of almost 30 years at a cafe near their home in the South Kensington neighborhood of London. He didn’t show. When she returned home, she found his body hanging from the leash attached to a door. In a dog bed, he’d left suicide notes, including one addressed to Jain, his longtime colleague.

The New York Post reported last year that the note to Jain contained an apology. A summary of Deutsche Bank’s own review of the suicide, seen by Bloomberg Businessweek, doesn’t mention the note and says the review found no direct link between Broeksmit’s death and his work at Deutsche.

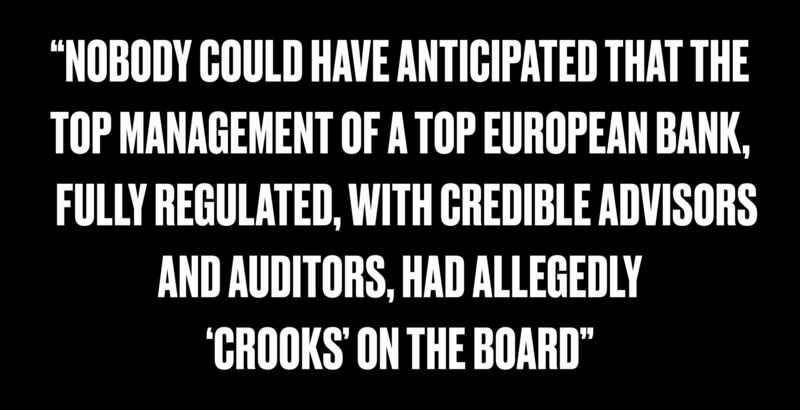

BaFin’s auditors interviewed Faissola on Aug. 28, 2014. He told them he couldn’t recall details of the period in which the Santorini deal closed. Faissola also said he couldn’t recall telling Deutsche’s lawyers in 2012 that the transaction could be characterized as “window dressing” Paschi’s financials, as another source had told the investigators.

Faissola laid blame on Paschi and defended his role.

“Nobody could have anticipated that the top management of a top European bank, fully regulated, with credible advisors and auditors, had allegedly ‘crooks’ on the board,” he told auditors hired by BaFin.

Faissola left Deutsche Bank in 2015, as did Jain and his co-CEO, Jürgen Fitschen. (Neither Jain nor Fitschen is accused in the Italian case.)

In February 2016, Deutsche said BaFin had closed its inquiries into Paschi and other matters, pointing to changes the bank had implemented and further measures it planned to take. An overhaul of the management board and the departure of senior executives contributed to the regulator’s assessment that the company had done enough, a person with knowledge of the matter said at the time.

On Oct. 1, 2016, a judge in Milan handed down his indictment in the Santorini affair.

The trial, which began with an initial hearing in December, is expected to run throughout 2017. Doubts about the financial health of Deutsche Bank have eased, but the stock is still about 80 percent below its 2007 high, and with legal costs uncertain, management hasn’t ruled out needing to raise more capital.

New CEO Cryan is expected to introduce a strategy as soon as February, when the bank announces its final 2016 results, which analysts estimate will barely show a profit. Brought in to right the ship, Cryan has been contrite.

“We didn’t always control ourselves,” he said at a Davos panel on Jan. 17. And those big bonuses? Gone. Senior employees won’t be getting any for the last year.

Meanwhile, Paschi is about to be nationalized in the biggest bank takeover by the state since the 1930s. And Faissola has kept busy. After his resignation he founded an investment company, based in Jersey in the Channel Islands, called F.A.B. Partners. The F stands for Faissola. It counts among its clients the Qatari government. With a stake of almost 10 percent, the regime is the biggest shareholder in Deutsche Bank.

According to recent reports, Faissola’s latest project is advising the Qataris on whether to boost that position—and extend his former employer a lifeline.

UPDATE:

According to the BaFin report, a sales unit (independent from the rates group) formally presented the transaction for approval to the Global Market Risks Assessment Committee on Dec. 1, 2008.

The committee, which included legal, compliance, and accounting unit members, was presented with Paschi’s economic rationale for the transaction before approving it. Regarding the Italian client’s accounting for these transactions, the BaFin report concluded that under German legal principles, none of Deutsche’s employees acted with the intent to aid Paschi in any misrepresentations of its balance sheet.

BaFin closed its inquiry in February 2016, and said it took no further action against Deutsche or its employees.

Pingback: Deutsche Bank: Was it Murder or Was It Suicide? - Why Deutsche Bank and Wall St. Conspired Against America