LIT UPDATE 2024

JAN 18, 2024

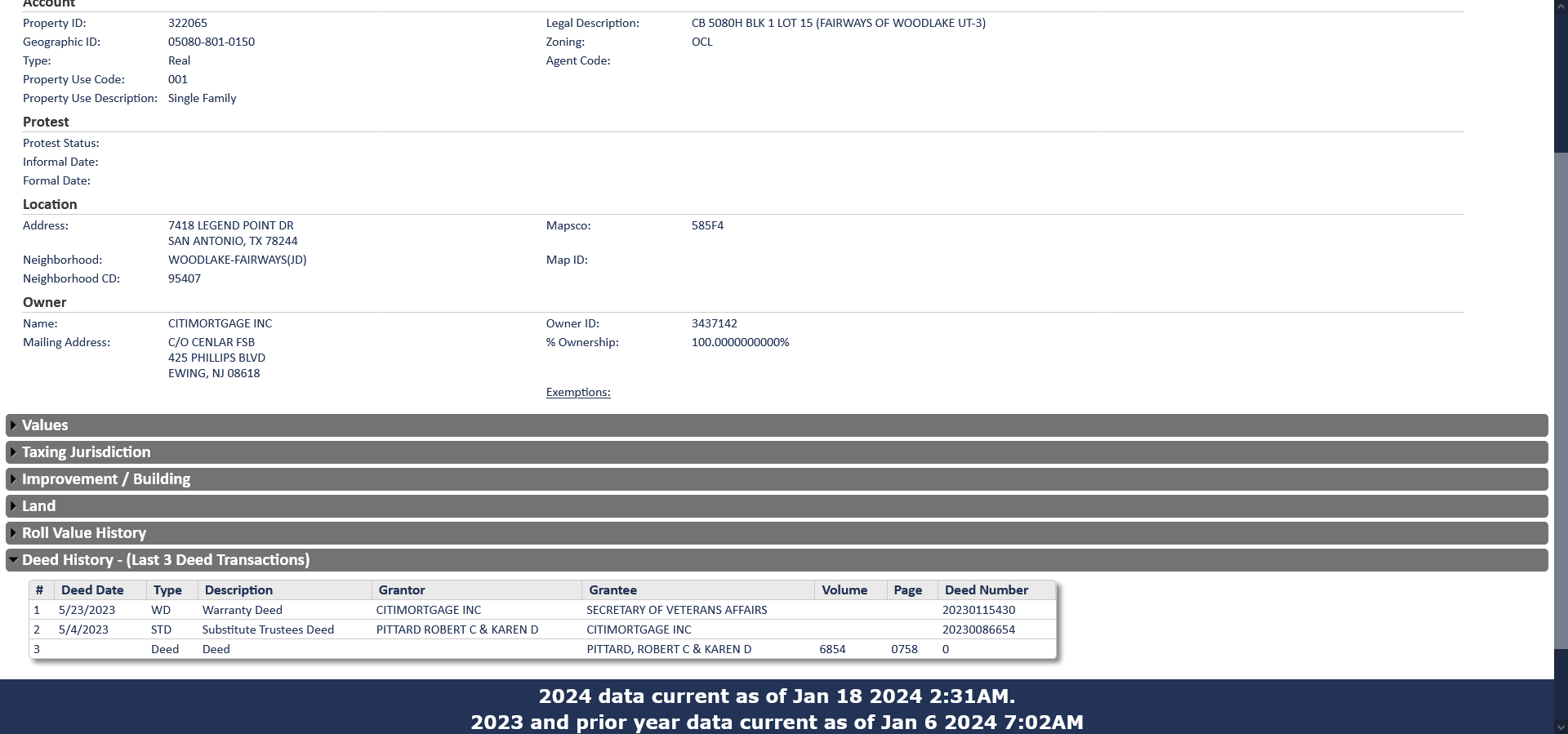

On May 4, 2023, Bexar CAD shows that the foreclosure sale completed 5/4/2023 and the home is now with the Cenlar FSB (Citi).

Pittard v. CitiMortgage, Inc.

(5:19-cv-01370)

District Court, W.D. Texas

NOV 25, 2019 | REPUBLISHED BY LIT: JUN 11, 2022

Despite judgment in 2020, Bexar county property tax records show that the Pittards’ are still in the residence which forms part of this wrongful foreclosure lawsuit, the Prittards’ 3rd lawsuit in a short timespan.

| CLOSED |

U.S. District Court [LIVE]

Western District of Texas (San Antonio)

CIVIL DOCKET FOR CASE #: 5:19-cv-01370-XR

| Pittard et al v. CitiMortgage, Inc. et al Assigned to: Judge Xavier Rodriguez

Cause: 28:1444 Petition for Removal- Foreclosure |

Date Filed: 11/21/2019 Date Terminated: 07/24/2020 Jury Demand: None Nature of Suit: 220 Real Property: Foreclosure Jurisdiction: Diversity |

| Plaintiff | ||

| Robert C. Pittard | represented by | John Evaristo Serna Law Offices of John E. Serna 3010 Hillcrest Drive San Antonio, TX 78201 (210) 833-6917 Fax: 210-733-7889 TERMINATED: 01/31/2020 LEAD ATTORNEY ATTORNEY TO BE NOTICEDR. Chris Pittard 1777 NE Loop 410, Suite 600 San Antonio, TX 78217 (210) 273-5578 Fax: (210) 820-2609 Email: chris_karen_pittard@yahoo.com LEAD ATTORNEY ATTORNEY TO BE NOTICED |

| Plaintiff | ||

| Karen D. Pittard | represented by | John Evaristo Serna (See above for address) TERMINATED: 01/31/2020 LEAD ATTORNEY ATTORNEY TO BE NOTICEDR. Chris Pittard (See above for address) LEAD ATTORNEY ATTORNEY TO BE NOTICED |

| V. | ||

| Defendant | ||

| CitiMortgage, Inc. | represented by | Crystal Gee Gibson Barrett Daffin Frappier Turner & Engel, LLP 4004 Belt Line Road, Suite 100 Addison, TX 75001 (972) 386-5040 Fax: (972) 341-0734 Email: crystalR@bdfgroup.com ATTORNEY TO BE NOTICED |

| Defendant | ||

| Cenlar FSB | represented by | Crystal Gee Gibson (See above for address) ATTORNEY TO BE NOTICED |

| Date Filed | # | Docket Text |

|---|---|---|

| 11/25/2019 | 3 | ANSWER to Complaint by Cenlar FSB, CitiMortgage, Inc..(Gibson, Crystal) (Entered: 11/25/2019) |

| 11/26/2019 | 4 | Order for Scheduling Recommendations/Proposed Scheduling Order. ( Scheduling Recommendations/Proposed Scheduling Order due by 12/30/2019,), Notice of right to consent to disposition of a civil case by a U.S. Magistrate Judge. Signed by Judge Xavier Rodriguez. (bc) (Entered: 11/26/2019) |

| 01/03/2020 | 5 | ORDER TO SHOW CAUSE as to Cenlar FSB, CitiMortgage, Inc., Karen D. Pittard, Robert C. Pittard., (Proposed Scheduling Order due by 1/17/2020) Show Cause Response due by 1/17/2020. Signed by Judge Xavier Rodriguez. (rg) (Entered: 01/06/2020) |

| 01/15/2020 | 6 | Rule 26(f) Discovery Report/Case Management Plan by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) (Entered: 01/15/2020) |

| 01/15/2020 | 7 | Scheduling Recommendations by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) (Entered: 01/15/2020) |

| 01/15/2020 | 8 | CONSENT to Trial by US Magistrate Judge by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) (Entered: 01/15/2020) |

| 01/16/2020 | 9 | ORDER SETTING STATUS CONFERENCE ( Status Conference set for 2/19/2020 10:30 AM before Judge Xavier Rodriguez). Signed by Judge Xavier Rodriguez. (bc) (Entered: 01/16/2020) |

| 01/16/2020 | 10 | SCHEDULING ORDER: Bench Trial set for 12/14/2020 10:30 AM before Judge Xavier Rodriguez. Final Pretrial Conference set for 12/3/2020 10:30 AM before Judge Xavier Rodriguez. ADR Report Deadline due by 7/15/2020, Amended Pleadings due by 3/3/2020, and Discovery due by 7/31/2020. Signed by Judge Xavier Rodriguez. (bc) (Entered: 01/16/2020) |

| 01/17/2020 | 11 | NOTICE of Attorney Appearance by R. Chris Pittard on behalf of Karen D. Pittard, Robert C. Pittard. Attorney R. Chris Pittard added to party Karen D. Pittard(pty:pla), Attorney R. Chris Pittard added to party Robert C. Pittard(pty:pla) (Pittard, R.) (Entered: 01/17/2020) |

| 01/30/2020 | 12 | Unopposed MOTION to Withdraw as Attorney for Plaintiffs by John E. Serna by Cenlar FSB, CitiMortgage, Inc.. (Attachments: # 1 Proposed Order)(Gibson, Crystal) (Entered: 01/30/2020) |

| 02/17/2020 | 13 | ***DOCUMENT DEFICIENT- MISSING A PROPOSED ORDER. PLEASE FILE THE PROPOSED ORDER AS A ATTACHMENT AND LINK TO THE ORIGINAL FILING.*** Opposed MOTION to Continue Pre-trial Conference by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) Modified on 2/18/2020 To edit text (bc). (Entered: 02/17/2020) |

| 02/18/2020 | 14 | DEFICIENCY NOTICE: ***DOCUMENT DEFICIENT- MISSING A PROPOSED ORDER. PLEASE FILE THE PROPOSED ORDER AS A ATTACHMENT AND LINK TO THE ORIGINAL FILING*** re 13 Opposed MOTION to Continue Pre-trial Conference (bc) (Entered: 02/18/2020) |

| 02/18/2020 | 15 | ATTACHMENT proposed order to 13 Opposed MOTION to Continue Pre-trial Conference by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) (Entered: 02/18/2020) |

| 02/27/2020 | 16 | Minute Entry for proceedings held before Judge Xavier Rodriguez: Status Conference held on 2/27/2020 (Minute entry documents are not available electronically.). (Court Reporter Gigi Simcox.)(bc) (Entered: 02/27/2020) |

| 03/12/2020 | 17 | AMENDED COMPLAINT against All Plaintiffs amending, filed by Robert C. Pittard, Karen D. Pittard.(Pittard, R.) (Entered: 03/12/2020) |

| 05/08/2020 | 18 | AMENDED ANSWER to 17 Amended Complaint by Cenlar FSB, CitiMortgage, Inc.. (Gibson, Crystal) (Entered: 05/08/2020) |

| 06/08/2020 | 19 | MOTION for Summary Judgment by Cenlar FSB, CitiMortgage, Inc.. (Attachments: # 1 Proposed Order)(Gibson, Crystal) (Entered: 06/08/2020) |

| 06/08/2020 | 20 | BRIEF regarding 19 MOTION for Summary Judgment by Cenlar FSB, CitiMortgage, Inc.. (Attachments: # 1 Exhibit A-2017 Petition, # 2 Exhibit B-Order Dismissing, # 3 Exhibit C-2018 Petition, # 4 Exhibit D-2019 Show Cause, # 5 Exhibit E-2019 Dismissal Order, # 6 Exhibit F-Pittard email-loan mod)(Gibson, Crystal) (Entered: 06/08/2020) |

| 06/22/2020 | 21 | Unopposed MOTION for Extension of Time to File Response/Reply as to 19 MOTION for Summary Judgment by Karen D. Pittard, Robert C. Pittard. (Pittard, R.) (Entered: 06/22/2020) |

| 06/25/2020 | 22 | Response in Opposition to Motion, filed by Karen D. Pittard, Robert C. Pittard, re 19 MOTION for Summary Judgment filed by Defendant Cenlar FSB, Defendant CitiMortgage, Inc. (Attachments: # 1 Exhibit Exhibit List, # 2 Exhibit, # 3 Exhibit, # 4 Exhibit, # 5 Exhibit, # 6 Exhibit, # 7 Exhibit, # 8 Exhibit, # 9 Exhibit, # 10 Exhibit, # 11 Exhibit, # 12 Exhibit, # 13 Exhibit, # 14 Exhibit, # 15 Exhibit)(Pittard, R.) (Entered: 06/25/2020) |

| 07/24/2020 | 23 |

ORDER GRANTING 19 Motion for Summary Judgment. The Clerk is DIRECTED to enter judgment in favor of Defendants and against Plaintiffs. Plaintiffs shall take nothing by their claims. Signed by Judge Xavier Rodriguez. (bc) (Entered: 07/27/2020) |

| 07/24/2020 | 24 | CLERK’S JUDGMENT (bc) (Entered: 07/27/2020) |

| PACER Service Center | |||

|---|---|---|---|

| Transaction Receipt | |||

| 06/11/2022 19:49:40 |

ORDER ON MOTION FOR SUMMARY JUDGMENT

On this date, the Court considered Defendants’ motion for summary judgment (docket no. 19), Defendants’ brief in support of that motion (docket no. 20), and Plaintiffs’ response (docket no. 22).

After careful consideration, Defendants’ motion is GRANTED.

BACKGROUND

Plaintiffs Robert and Karen Pittard (collectively, “Plaintiffs”) bring this action against Defendants CitiMortgage, Inc. (“CMI”) and Cenlar FSB (“Cenlar”) (collectively, “Defendants”), asserting claims for breach of contract, fraud, and misrepresentation related to the financing of their home located at 7418 Legend Point Drive, San Antonio, Texas.

Docket no. 17.

Plaintiffs initially executed a note in the amount of $197,698.00 on March 6, 1998.

See Pittard v. CitiMortgage, Inc., 5:17-cv-118-DAE, docket no. 4-1 at 2.1

The note was made payable to Edlin Mortgage Company and provided that Plaintiffs would be in default if they did not meet the required monthly payments, which would thereafter allow the mortgagee to accelerate the note,

Criminal Case Update: Read this ORDER. Now you know what to expect at sentencing of Dallas Lawyer Ray Jackson (yeah, we know he’s still holdin’ out as a lawyer, it’s in his DNA). https://t.co/sOFQPkg9Wi @NDTXnews @uscourts @statebaroftexas @SupremeCourt_TX @TXAG @GregAbbott_TX

— lawsinusa (@lawsinusa) June 11, 2022

requiring the unpaid balance be paid immediately.

Id.

Plaintiffs also executed a deed of trust, held by CMI, which similarly authorizes the acceleration of the maturity date, and also allows the mortgagee to foreclose the property if Plaintiffs default.

Id. at docket no. 4-2.

Defendant Cenlar is the mortgage servicer for both the Note and the Deed of Trust.

This is not Plaintiffs’ first time in court seeking to prevent the foreclosure of the property.

There are three relevant lawsuits:one in 2017, one in 2018, and the present lawsuit which began in 2019.

Because the details of each suit are relevant to Defendants’ preclusion arguments, the Court addresses each suit here in detail.

A. First Lawsuit (2017)

In 2017 Plaintiffs brought suit against CMI in state court to prevent the foreclosure of their home.

Docket no. 20-1 at 3.

That suit alleged wrongful collection practices and wrongful foreclosure (or attempted wrongful foreclosure) and sought an accounting.

Id. at 4.

, Plaintiffs asserted that CMI

(1) failed to provide sufficient information to allow Plaintiffs to determine the amount owed;

(2) prematurely sought foreclosure and failed to comply with the Texas Property Code’s rules regarding notice of foreclosure sales;

(3) failed to credit all payments made, refused to accept other payments, and made improper and unauthorized charges;

and

(4) failed to make any reasonable effort to work with Plaintiffs to save the property, despite Plaintiffs’ substantial interest in that property.

Id. at 4–5.

In that suit, Plaintiffs denied being in default on their mortgage payments. Id. at 5.

CMI removed the action to federal court, and the case was assigned to U.S. District Judge David A. Ezra.

Docket no. 20-2.

CMI filed a motion to dismiss, to which Plaintiffs did not respond.

Id. at 3.

On April 13, 2017, Judge Ezra granted that motion to dismiss without prejudice.

For the claim of wrongful foreclosure, he found that

(1) Texas courts do not recognize an action for attempted wrongful foreclosure,

and

(2) a wrongful foreclosure claim cannot survive if the foreclosure had not actually occurred, which it had not.

Id. at 6.

Next, as to Plaintiffs’ claims for wrongful debt collection practices, the court found there were no allegations of any false, deceptive, or otherwise misleading debt collection practices.

Id. at 7–9.

Finally, with respect to the claim for an accounting, the court dismissed that claim—to the extent it was a cause of action rather than a remedy—because Plaintiffs failed to allege that they were unable to obtain the relevant information through ordinary discovery procedures.

Id. at 9–10.

Having thus dismissed each cause of action, Judge Ezra also dismissed the claim for injunctive relief due to failure to show a substantial likelihood of success on the merits.

Id. at 11.

B. Second Lawsuit (2018)

On November 2, 2018, Plaintiffs filed a second lawsuit in state court against CMI.

Docket no. 20-3.

This petition asserted a claim for breach of contract, alleging that CMI unlawfully declared default and accelerated the mortgage maturity date.

Plaintiffs claimed that they sent all required monies to Defendants but that the money was returned to them, upon which CMI sought foreclosure.

Id. at 5; see also docket nos. 22-7 at 2 (notice of default), 22-8 at 2 (proof of Plaintiffs’ payment of the requested amount), and 22-9 at 2 (“CMI’s return of the funds “because the amount is insufficient to cure your delinquency and your account is not under a payment plan”).

Thus, “despite the efforts of Plaintiff[s] to make payments of the note…[CMI] has insisted on the foreclosure of the mortgage…There is no default sufficient to justify foreclosure, and any alleged default has been cured or waived.”

Id. at 5–6.

Though unclear if brought as a second cause of action, the petition also asserted that CMI failed to exercise the implied covenant of good faith and fair dealing.

Id. at 4.

After Plaintiffs obtained a temporary restraining order, CMI removed again to federal court where the case was assigned to Chief U.S. District Judge Orlando L. Garcia.

Docket no. 20-4.

CMI filed a motion for judgment on the pleadings on January 31, 2019, and, again, Plaintiffs did not respond despite Chief Judge Garcia issuing a show cause order for Plaintiffs to explain why the motion should not be granted.

Id.

Eventually, Chief Judge Garcia granted that motion and dismissed the case under Fed. Rule Civ. P. 41(b) for failure to prosecute.

Docket no. 20-5 at 7.

As to the breach of contract claim, Judge Garcia found that “Plaintiffs have failed to plead any factual details regarding

(1) why their loan was not in default,

(2) how Plaintiffs allegedly cured their default,

and/or

(3) how Defendant failed to credit Plaintiffs’ payment towards their account.”

Id. at 5.

“[M]ore importantly,” he wrote, “Plaintiffs have failed to identify which actual contract or— assuming it is the promissory note and/or deed of trust that are mentioned in the petition—any specific provision of the actual contracts that Defendant allegedly breached.”

Id.

Nor did the petition “set forth the factual allegations demonstrating the manner in which Defendant allegedly breached the provision.”

Id.

He further found that Plaintiffs had not demonstrated any damages from the alleged breach, given that they previously obtained a restraining order precluding the foreclosure sale.

Id. at n. 2.

Finally, to the extent Plaintiffs brought the breach of the implied covenant of good faith and fair dealing as a separate cause of action, Chief Judge Garcia found that “Texas courts have routinely held that the ‘relationship of mortgagor and mortgagee ordinarily does not involve a duty of good faith.’”

Id. at 6 (citing Motten v. Chase Home Fin., 831 F. Supp. 2d 988, 1004 (S.D. Tex. 2011)).

Further, Plaintiffs did not explain how that covenant applied to their loan or how CMI violated the covenant.

Id.

As Judge Ezra had, Chief Judge Garcia also dismissed the request for injunctive relief because injunctive relief requires a viable cause of action, which Plaintiffs’ petition did not have.

Id.

In court unabashedly with a bankruptcy petition, when Thievin’ Texas Lawyer Chris Pettit should be in Shackles and Orange before a Federal Judge under Criminal Indictment. Allegedly he Stole Tens of Millions from clients. This is why Lawyers Trust Accounts need Externally Audited https://t.co/4kJniJp9xL pic.twitter.com/00lqkRtU4W

— lawsinusa (@lawsinusa) June 6, 2022

C. Third (and present) Lawsuit (2019)

Plaintiff’s brought their third lawsuit in state court on November 1, 2019, this time asserting claims against both CMI and Cenlar FSB, the mortgage servicer.

Docket no. 1-1 at 8.

The state court granted the requested temporary restraining order, id. at 5, though there were no causes of action asserted in the underlying petition.

After CMI again removed the case to this Court, at a status conference on February 27, 2020, this Court ordered Plaintiffs to file an amended complaint that alleges an actual underlying cause of action.

See docket no. 16.

On May 5, 2020, Plaintiffs filed that amended complaint, now asserting claims for breach of contract and fraud/misrepresentation.

Docket no. 17.

This iteration of the lawsuit began to prevent the foreclosure of the property which was originally set for November 5, 2019.

Docket no. 17.

Plaintiffs assert that on June 25, 2019, they requested a loan remodification package from CMI through its servicing agent, Cenlar FSB.

Docket no. 22-2 at 11; no. 22-13 at 2

(“[W]e would like an accounting as to where the loan currently is, and what we can do to make up the arrearages and get back on track in repaying the loan.”).

Plaintiffs, in an affidavit attached to their initial request for a restraining order, allege that Cenlar FSB advised Plaintiffs that “they would be willing to work with us in reinstating or re- modifying the mortgage.”

Docket no. 22-2 at 11.

They claim Cenlar “did not send [the modification package] until after August 12, 2019, and subsequently on September 10, 2019, initiated steps to foreclose on the property in question.”

Id.

Thereafter, Plaintiff Robert Pittard suffered a stroke and was hospitalized for several days.

Id.

He claims that neither he nor his wife, Plaintiff Karen Pittard, who was acting as his caretaker, “had the time or the opportunity to attempt to refinance or bring the account current before the property was foreclosed and set for auction sale.”

Id. at 12.

His affidavit further states that he “was never served with or given adequate and sufficient notice” of the intent to foreclose, and that he “was never notified or informed of the total amount of the arrearage and delinquency on my account

Id.2

The First Amended Complaint in this case asserts two causes of action: breach of contract and fraud/misrepresentation.

The breach of contract claim is described as follows:

Defendants’ conduct as described above amounts to a breach of contract.

Defendants are required to provide adequate notice of he [sic] intent to foreclose.

In this case, Plaintiffs allege that Defendants failed to provide adequate notice.

Docket no. 17 at 3.

The fraud and misrepresentation claim states that:

Defendants engaged in fraudulent activity when they offered to assist Plaintiffs in potentially saving their home through loan re-modification; however, at the same time, Defendants initiated foreclosure proceedings with the intent of foreclosing on Plaintiffs’ home without giving Plaintiffs adequate time to engage in the re- modification process.

The situation was exacerbated by Plaintiff’s medical emergency, giving Plaintiffs even less opportunity to participate in the re- modification process.

Id. at 3–4.

DISCUSSION

I. Standard of Review

The Court shall grant summary judgment if the movant shows that there is no genuine dispute as to any material fact and the movant is entitled to judgment as a matter of law.

FED. R. CIV. P. 56.

To establish that there is no genuine issue as to any material fact, the movant must either submit evidence that negates the existence of some material element of the non-moving party’s claim or defense, or, if the crucial issue is one for which the non-moving party will bear

Legal Team

We stand for expertise and years of experience in a wide variety of legal disciplines. Get to know us better.

R. Chris Pittard

Attorney

Legal Field:

Employment Law

Employment Discrimination

Federal Sector EEO Cases

Wills

Contracts

Professional Education:

1977, Bachelor of Arts in History, University of Texas, Austin, TX

1980, U.S. Army Airborne and Ranger Schools, Ft. Benning, GA

1991, U.S. Army Command and General Staff College, KS

1991, Masters Military Arts and Science, U.S. Army C&GSC, KS

1995, Juris Doctor, Cum Laude, St. Mary’s University Law School, San Antonio, TX

1996, Certified Bexar County Community Mediator

Profssional Experience:

U.S. Army Infantry Officer, 1979-1992

Attorney, Ball & Weed, P.C., 1995-1996

Attorney, Phil Watkins, P.C., 1996-1998

Adjunct Professor, St. Mary’s University School of Law, 1996-2004

Sr. Trial Attorney, EEOC, 1998-2002

Owner, Law Office R. Chris Pittard, 2002-2005

Attorney, Davis Law Firm, 2005-2007

Director, Employment Law Dept., Davis Law Firm, 2007-2009

Shareholder, Forte & Pittard, P.L.L.C., 2010 to present

Author, Transmanaut Chronicles, Prosperity Publications, 2014

Memberships:

Admitted to United States Supreme Court, 2016

Admitted to Texas State Bar, 1995

Admitted to Western District of Texas, 1997

Admitted to Southern District of Texas, 1999

Admitted to U. S. Appeals Court for the Fifth Circuit, 2003

San Antonio Black Lawyers Association Member

Member Texas State Bar Employment Section

Named one of Texas Best Lawyers in 2011, 2013 Labor and Employment Law

Named one of Texas Top-Rated Lawyers in 2012, Labor & Employment LawProgram Advisory Committee member, Brown Mackie College

Robert Forte

Attorney

Specializations:

Formation and Transactions

Tax Resolution

Estate Law

Professional Education:

1989, Bachelors of Art, University of Texas, Austin, TX

1995, Juris Doctorate, St. Mary’s University School of Law, San Antonio, TX

Professional Experience:

Investigator, Protective and Regulatory Services, 1990 to 1992, 1995 to 1998

Owner, Music Management Company, 1998 to 2003

Owner, Law Office of Robert Forte, 2003 to 2010

Shareholder, Forte & Pittard, P.L.L.C., 2010 to present

Memberships:

Admitted to State Bar of Texas, 2003

Member Texas State Bar Sports Law and Entertainment Section

Member Texas State Bar Litigation Section

the burden of proof at trial, merely point out that the evidence in the record is insufficient to support an essential element of the non-movant’s claim or defense.

Little v. Liquid Air Corp., 952 F.2d 841, 847 (5th Cir. 1992), on reh’g en banc, 37 F.3d 1069 (5th Cir. 1994) (citing Celotex Corp. v. Catrett, 477 U.S. 317, 323 (1986)).

Once the movant carries its initial burden, the burden shifts to the non-movant to show that summary judgment is inappropriate.

See Fields v. City of S. Hous., 922 F.2d 1183, 1187 (5th Cir. 1991).

Any “[u]nsubstantiated assertions, improbable inferences, and unsupported speculation are not sufficient to defeat a motion for summary judgment,” Brown

v. City of Houston, 337 F.3d 539, 541 (5th Cir. 2003), and neither will “only a scintilla of evidence” meet the nonmovant’s burden.

Little v. Liquid Air Corp., 37 F.3d 1069, 1075 (5th Cir. 1994) (en banc).

Rather, the nonmovant must “set forth specific facts showing the existence of a ‘genuine’ issue concerning every essential component of its case.”

Morris v. Covan World Wide Moving, Inc., 144 F.3d 377, 380 (5th Cir. 1998).

The Court will not assume “in the absence of any proof…that the nonmoving party could or would prove the necessary facts” and will grant summary judgment “in any case where critical evidence is so weak or tenuous on an essential fact that it could not support a judgment in favor of the nonmovant.”

Little, 37 F.3d at 1075.

For a court to conclude that there are no genuine issues of material fact, the court must be satisfied that no reasonable trier of fact could have found for the non-movant, or, in other words, that the evidence favoring the non-movant is insufficient to enable a reasonable jury to return a verdict for the non-movant.

See Anderson v. Liberty Lobby, Inc., 477 U.S. 242, 248 (1986).

In making this determination, the court should review all the evidence in the record, giving credence to the evidence favoring the non-movant as well as the “evidence supporting the moving party that is uncontradicted and unimpeached, at least to the extent that evidence comes from disinterested witnesses.”

Reeves v. Sanderson Plumbing Prods., Inc., 530 U.S. 133, 151 (2000).

The Court “may not make credibility determinations or weigh the evidence” in ruling on a motion for summary judgment, id. at 150, and must review all facts in the light most favorable to the non-moving party.

First Colony Life Ins. Co. v. Sanford, 555 F.3d 177, 181 (5th Cir. 2009).

Disgraced and Disbarred: Why Are Former Judges and Lawyers Working as Mediators in Our Courts? – https://t.co/qFFC0Yl4kb

— lawsinusa (@lawsinusa) June 11, 2022

II. Analysis

Defendants raise three separate arguments in their motion for summary judgment.

First, claim preclusion—or res judicata—bars this entire lawsuit because this lawsuit involves the “same subject matter” as the previous two suits.

Docket no. 20 at 9–12.

Similarly, Defendants argue that issue preclusion—or collateral estoppel—precludes the relitigation of issues in this case that were already litigated in the prior actions.

Alternatively, Defendants argue that both the breach of contract claim, and the fraud/misrepresentation claim fail under ordinary state-law principles.

Docket no. 20 at 13–17.

The Court will address each argument in turn.

A. Claim Preclusion

Defendants first argue that claim preclusion, or res judicata, requires dismissal of all of Plaintiffs’ claims.

Docket no. 20 at 9–12.

They assert that the second lawsuit constitutes a final judgment on the merits and that the third and current lawsuit is “based on the same claim or claims that were, or could have been litigated in the prior three3 lawsuits as the subject matter of both lawsuits is the same.”

Id. at 11.

Defendants claim that “the subject matter of all three lawsuits are clearly and without question, the Property, the mortgage loan (and its accounting), the validity of CMI’s lien, and Defendants’ ability to foreclose.”

Id. (emphasis in original).

Plaintiffs respond that res judicata is inapplicable “because each matter is distinguishable from the others,” and that although “each matter concerned Plaintiffs’ home, they are based on different facts over a three-

year period.

They are not a continuing lawsuit,” but rather “each one is unique….”

Docket no. 22 at 5.

The doctrine of res judicata contemplates, at minimum, that courts not be required to adjudicate, nor defendants to address, successive actions arising out of the same transaction.

Nilsen v. City of Moss Point, Miss., 701 F.2d 556, 563 (5th Cir. 1983).

For a claim to be barred on res judicata grounds, the Fifth Circuit requires that:

(1) the parties are identical or in privity;

(2) the judgment in the prior action was rendered by a court of competent jurisdiction;

(3) the prior action was concluded by a final judgment on the merits;

and

(4) the same claim or cause of action was involved in both actions.

Test Masters Educ. Servs., Inc. v. Singh, 428 F.3d 559, 571 (5th Cir. 2005).4

When those elements are satisfied, res judicata “prohibits either party from raising any claim or defense in the later action that was or could have been raised in support of or in opposition to the cause of action asserted in the prior action.”

United States v. Shanbaum, 10 F.3d 305, 310 (5th Cir. 1994) (emphasis in original);

see also In re Air Crash at Dallas/Fort Worth Airport on Aug. 2, 1985, 861 F.2d 814, 816 (5th Cir. 1988)

(“Res judicata extends to matters that should have been raised in the earlier suit as well as those that were.”).

As to the last element—whether the same claim or cause of action was involved in both actions—courts apply a “transactional test, which requires that the two actions be based on the same nucleus of operative facts.”

Oreck Direct, LLC v. Dyson, Inc., 560 F.3d 398, 402 (5th Cir.

2009) (internal citations omitted).

The preclusive effect of a prior judgment extends “to all or any part of the transaction, or series of connected transactions, out of which the original action arose.”

Id.

Under that transactional test, a prior judgment’s preclusive effect extends to all rights the original plaintiff had “with respect to all or any part of the transaction, or series of connected transactions, out of which the [original] action arose.”

Petro-Hunt, L.L.C. v. United States, 365 F.3d 385, 395–96 (5th Cir. 2004).

Courts “pragmatically” determine what facts constitute a transaction by considering factors like “whether the facts are related in time, space, origin, or motivation, whether they form a convenient trial unit, and whether their treatment as a unit conforms to the parties’ expectations or business understanding or usage.”

Id. at 396.

“The nucleus of operative facts, rather than the type of relief requested, substantive theories advanced, or types of rights asserted, defines the claim.”

United States v. Davenport, 484 F.3d 321, 326 (5th Cir. 2007).

Additionally, the doctrine “extends beyond claims that were actually raised and bars all claims that ‘could have been advanced in support of the cause of action on the occasion of its former adjudication….’”

Maxwell v. U.S. Bank, N.A., 544 F. App’x 470, 472 (5th Cir. 2013) (quoting In re Howe, 913 F.2d 1138, 1144 (5th Cir. 1990)).

Finally, the res judicata doctrine does not bar plaintiffs “from presenting any ground for relief arising out of conduct not complained of in the prior lawsuits.”

Kilgoar v. Colbert Cty. Bd. of Educ., 578 F.2d 1033, 1035 (5th Cir. 1978).

“Subsequent conduct, even if it is of the same nature as the conduct complained of in a prior lawsuit, may give rise to an entirely separate cause of action.”

Id.;

see also Alwais v. New Penn Fin., LLC, No. SA-18-CV-604-XR, 2019 WL 1004857, at *3 (W.D. Tex. Mar. 1, 2019)

(denying similar motion because the “[p]laintiff could not have brought any claims related to these acts in the prior suit because they had not yet happened.”).

The parties do not dispute that

(1) the parties are identical or in privity,5 or that

(2) the judgments in the prior acts were rendered by a court of competent jurisdiction.

The disputed elements are the third and fourth: whether the prior actions were concluded by a final judgment on the merits, and whether the same claim or cause of action was involved in the prior and current lawsuit.

ii. Were the prior decisions “final judgments on the merits”?

Beginning with whether the prior lawsuits were “final judgments on the merits,” the first lawsuit was not but the second was.

The 2017 lawsuit ended when Judge Ezra dismissed the case without prejudice.

Such a dismissal “without prejudice” does not “operat[e] as an adjudication upon the merits” and thus does not have a res judicata effect.

Cooter & Gell v. Hartmarx Corp., 496 U.S. 384, 396 (1990);

Am. Heritage Life Ins. Co. v. Heritage Life Ins. Co., 494 F.2d 3, 9 (5th Cir. 1974).

The second lawsuit, however, ended when Chief Judge Garcia dismissed the case pursuant to Rule 41(b).

That rule concerns involuntary dismissals and their effects.

It provides that “[u]nless the dismissal order states otherwise, a dismissal under this subdivision…operates as an adjudication on the merits.”

FED. R. CIV. P. 41(b).

However, in Semtek Int’l v. Lockheed Martin Corp., 531 U.S. 497, 501 (2001), the Supreme Court cautioned that the language in Rule 41(b) does not necessarily mean that claim preclusion applies.

See also Vasquez v. Bridgestone/Firestone, Inc., 325 F.3d 665, 678 (5th Cir. 2003)

(“[A]n ‘adjudication on the merits’ [under Rule 41(b)] bars refiling of the same claim in the same court but does not establish claim preclusion.”) (emphasis added).

Accordingly, the Court “must look to federal common law to determine the claim preclusive effect of the prior judgment of the federal court.”

Cano v. Everest Minerals Corp., No. SA-01-CA-610-XR, 2004 WL 502628, at *6 (W.D. Tex. Mar. 10, 2004)

(considering federal common law to determine preclusive effect of a Rule 41(b) dismissal);

see also Vasquez, 325 F.3d at 679

(“We look to the longstanding rule that federal common law governs the claim-preclusive effect of a dismissal by a federal court sitting in diversity.”).

Specifically, the Court must determine the preclusive effect given to judgments issued for failure to prosecute.

Courts indeed generally treat dismissals for failure to prosecute as “final judgments on the merits” for claim preclusion purposes.

See WRIGHT, MILLER & COOPER, FED. PRAC. & PROC. § 4440

(“Many of the cases involving the preclusive effects of penalty dismissals arise from failure to prosecute a prior action. Preclusion has been applied in such cases even though the plaintiff was not clearly to blame for the failure.”) (collecting cases);

see also Adame v. UETA Inc., No. L-04-93, 2005 WL 1249262, at *1 (S.D. Tex. Apr. 25, 2005)

(finding that a dismissal for want of prosecution “has the res judicata effect of barring any adjudication on [the plaintiff’s] instant suit”).

Accordingly, Chief Judge Garcia’s dismissal under Rule 41(b) acts as a final judgment on the merits for res judicata purposes.

ii. Was the same claim or cause of action involved in the prior suits?

With the first three elements satisfied, the Court must determine whether the same claim or cause of action was involved in the second lawsuit and this one.

As to the breach of contract claim, while it is true that Plaintiffs brought such a claim in both lawsuits, the basis for the claims differs under each lawsuit.

In the first lawsuit, the breach of contract claim was premised on Defendants’ alleged failure to consider Plaintiffs’ curing of any default or, alternatively, that there was “no default sufficient to justify foreclosure.”

Docket no. 20-3 at 6.

In this lawsuit, however, the breach of contract is premised on Defendants’ alleged failure to provide adequate notice of the intent to foreclose.

Docket no. 17 at 3.

Defendants assertion that Plaintiffs could have brought this same claim in the prior actions is foreclosed by the fact that the deficient notices Plaintiffs complain of here concern the foreclosure that was scheduled for November 5, 2019—after the conclusion of the prior lawsuit.

See docket no. 20-5 at 7 (dismissing case on May 22, 2019).

The alleged conduct was subsequent to the prior action and though it is “of the same nature as the conduct complained of” in the second lawsuit, Plaintiffs could not have brought any claims related to the lack of foreclosure notice in November 2019 because the judgment in the prior suit preceded that foreclosure by several months.

Kilgoar, 578 F.2d at 1035; Alwais, 2019 WL 1004857, at *3

(“Plaintiff could not have brought any claims related to these acts in the prior suit because they had not yet happened.”).

The same applies to the fraud/misrepresentation claim.

The fact that Plaintiffs did not previously bring a fraud/misrepresentation claim does not, itself, prevent claim preclusion from applying.

See Davenport, 484 F.3d at 326 (“The nucleus of operative facts, rather than the type of relief requested, substantive theories advanced, or types of rights asserted, defines the claim.”).

But here, as with the breach of contract claim, the nucleus of operative facts underlying the claim is distinct from anything asserted in the prior action because the complained of conduct— Defendants’ misrepresentation regarding their intent to modify the loan—took place after the second lawsuit and, thus, could not have been brought in that action.

Kilgoar, 578 F.2d at 1035; Alwais, 2019 WL 1004857, at *3.

Accordingly, neither Plaintiffs’ breach of contract claim nor their fraud/misrepresentation claim is barred under claim preclusion principles.

His Dad may have been a Judge, but this Texas Lawyer and Firm is not licensed in the State with the Texas OCCC as a debt settlement agency. https://t.co/K3WD5JYxzz

— lawsinusa (@lawsinusa) June 6, 2022

B. Issue Preclusion

Defendants next assert that issue preclusion applies to bar certain issues raised in Plaintiffs’ complaint. Docket no. 20 at 12–13.

They assert that Plaintiffs’ first lawsuit brought claims for wrongful foreclosure, breach of contract for failure to provide proper notice under the Deed of Trust, Texas Property Code violations with regard to the notice of sale, failure to provide a proper accounting, and failure to “work with” Plaintiffs to save their property.

Id. at 12.

The second lawsuit also asserted a breach of contract claim, again alleging that CMI failed to maintain a proper accounting, and an assertion that Plaintiffs cured any default.

Id.

The present lawsuit brings claims for breach of contract and fraud/misrepresentation, premised on Defendants’ alleged refusal to allow Plaintiffs to refinance, renegotiate, or reinstate their mortgage, and their offer to assist in saving the property but initiation of foreclosure before engaging in that promised modification process.

Id. at 13.

Plaintiffs respond to Defendants’ issue preclusion arguments in the same way:

“Collateral estoppel do[es] not apply because each matter is distinguishable from the others.”

Issue preclusion, or collateral estoppel, “precludes a party from litigating an issue already raised in an earlier action between the same parties if:

(1) the issue at stake is identical to the one involved in the earlier action;

(2) the issue was actually litigated in the prior action;

and

(3) the determination of the issue in the prior action was a necessary part of the judgment in that action.”

Petro-Hunt, 365 F.3d at 397.

The doctrine “does not preclude litigation of an issue unless both the facts and the legal standard used to assess them are the same in both proceedings.”

Copeland v. Merrill Lynch & Co., Inc., 47 F.3d 1415, 1422 (5th Cir. 1995).6

The analysis here is similar to the claim preclusion analysis.

Simply put, the conduct complained of here is conduct that occurred after the previous litigation, so the issues relevant here cannot have logically been identical, actually litigated, or determinative of the prior actions.

Though the breach of contract claim is nominally the same as the prior breach of contract claim, the issues and facts underlying that breach are different.

Plaintiffs now complain of the lack of notice for the foreclosure sale scheduled for November 5, 2019, conduct which occurred after the prior lawsuit terminated on May 22, 2019.

Docket no. 17 at 3–5.

Indeed, the facts asserted in Plaintiffs’ First Amended Complaint begin with the foreclosure sale scheduled for November 5.

Docket no. 17 at 2.

That is to say, Plaintiffs do not reallege any of the facts relevant to the prior actions, such as the previous failure to provide notice of the 2017 foreclosure.

Though the underlying contract itself may be the same, Plaintiffs allege a new breach of that contract, separate and apart from the breach previously asserted.

The same is true for the fraud/misrepresentation claim: Plaintiffs’ assertions here are for conduct that came after the prior lawsuit and, therefore, could not have been raised or litigated in the prior action.

Issue preclusion, therefore, does not bar any issues asserted in this lawsuit.

Kilgoar, 578 F.2d at 1035; see also Allergan Sales, LLC v. Sandoz, Inc., No. 12-cv-207-JRG, 2016 WL 1224868, at *5 (E.D. Tex. Mar. 29, 2016)

(finding issue preclusion inapplicable where conduct asserted occurred after termination of prior litigation).

Accordingly, claim preclusion does not bar Plaintiffs’ claims for breach of contract and fraud/misrepresentation, nor does issue preclusion bar any of the facts or issues upon which those claims are premised.

C. Breach of Contract

Defendants argue that even if Plaintiffs’ breach of contract claim survives their preclusion defense, that claim—the sole basis of which is the allegation that Defendants did not provide adequate notice of their intent to foreclose—fails as a matter of law.

Docket no. 20 at 13–15.

First, they argue that where borrowers like Plaintiffs are in default, they cannot assert a breach of contract claim.

Id. at 13–14.

Second, they argue that Plaintiffs have not shown they suffered any damages because they have not been dispossessed of their home—meaning that foreclosure is merely a speculative damage—and have not made any payments on the Loan Agreement.

Id. at 14–15. Thus, “when the lien holder complied with the terms of the contract (as is the case here), and the plaintiff cannot demonstrate any damages, a breach-of-contract claim cannot stand.”

Id. at 15.

In their response, Plaintiffs do not assert any arguments regarding their breach of contract claim.

Under Texas law, applicable to this diversity action, “the elements in a breach of contract claim include:

(1) the existence of a valid contract;

(2) that the plaintiff performed or tendered performance;

(3) that the defendant breached the contract;

and

(4) that the plaintiff was damaged as a result of the beach.”

Cordero v. Avon Prods., Inc., 629 F. App’x 620, 623 (5th Cir. 2015) (internal quotations omitted);

Hovorka v. Cmty. Health Sys., Inc., 262 S.W.3d 503, 508–09 (Tex.App.—El Paso 2008, no pet.).

In the mortgage context, “a party to a contract who is himself in default cannot maintain a suit for its breach.”

Gulf Pipe Line Co. v. Nearen, 138 S.W.2d 1065, 1068 (Tex. 1940); Water Dynamics, Ltd v. HSBC Bank USA, N.A., 509 F. App’x 367, 369 (5th Cir. 2013) (citing Dobbins v. Redden, 785 S.W.2d 377, 378 (Tex. 1990)).

Plaintiffs admit that their account was not current.

See docket no. 17 at 3

(“[Plaintiffs] did not have the time and opportunity to attempt to refinance or bring their account current before the property was foreclosed and set for auction.”).

Accordingly, Plaintiffs cannot maintain their breach of contract claim.

The breach of contract claim also fails because Plaintiffs have not alleged any damages, the fourth and final element of a breach of contract claim.

Hovorka, 262 S.W.2d at 508–09.

No foreclosure has occurred in this case, so Plaintiffs cannot show any damage from the alleged lack of notice of the foreclosure sale.

De La Mora v. CitiMortgage, Inc., No. 7:17-CV-468, 2015 WL 12803712, at *2 (S.D. Tex. Jan. 26, 2015)

(“Plaintiff cannot show damages resulting from any such breach because no foreclosure sale has occurred.”);

Adams v. U.S. Bank, N.A., No. 3:17-cv-723, 2018 WL 2164520, at *6 (N.D. Tex. Apr. 18. 2018)

(“[N]o foreclosure sale has occurred that would actually deprive [the plaintiff] of her property rights she alleges are threatened.”).7

Chief Judge Garcia previously dismissed Plaintiffs’ breach of contract claim, in part, for the very same reason.

See No. 5:18-CV-1181-OLG at docket no. 10, n.2

(“Plaintiffs have not suffered the loss of property rights because they previously obtained an ex parte restraining order that precluded a foreclosure sale…. Thus, Plaintiffs’ failure to adequately allege damages provides a second basis for dismissing Plaintiffs’ breach of contract claim on the merits.”).

Finally, Chief Judge Garcia further dismissed the breach of contract claim because Plaintiffs “failed to identify which actual contract or…any specific provision of the actual contracts that [CMI] allegedly breached.”

Id. at 4.

Plaintiffs’ First Amended Complaint in this case is similarly deficient in that it fails to identify what contract was allegedly breached and, even assuming it is the promissory note and/or deed of trust, which provision of that contract was breached.

See docket no. 17 at 3.

Accordingly, Plaintiffs’ breach of contract claim, though it survives the preclusion challenges, fails as a matter of law because Plaintiffs may not bring such a claim when they themselves are in default, because Plaintiffs have not shown any damages, and because Plaintiffs have failed to specify which contract and which provision they allege Defendants breached.

Right now they all believe as Judges and Lawyers, if they stick together they are ‘untouchable’. LIT agrees, the most dangerous branch the judiciary, has a valid argument, based on historical data. However, LIT suggests that data has dramatically changedhttps://t.co/kyOvYmdcGI

— lawsinusa (@lawsinusa) June 6, 2022

D. Fraud and Misrepresentation

Finally, Defendants argue that Plaintiffs’ claim for fraud and misrepresentation fails.

Docket no. 20 at 15–17.

Both claims—based on the allegation that Defendants offered a loan modification review but nonetheless proceeded with the foreclosure—fail for lack of writing under

the statute of frauds, and fail because the alleged fraudulent behavior here was a misrepresentation as to a “promise of future conduct” rather than “one of existing fact.”

Id. at 16.

Defendants further assert that there is “no evidence that [Plaintiffs] submitted a loan modification application” or that they actually failed to consider any such modification.

Id. at 17.

Finally, the claims fail because Plaintiffs cannot show they suffered any damages as a result of the fraudulent misrepresentation, given that they “continue to reside in the Property rent free and have done so since May 2016 without making a mortgage payment.”

Id.

To prevail on a claim for common law fraud,8 a plaintiff must show:

(1) [T]he defendant made a material representation that was false;

(2) the defendant knew the representation was false or made it recklessly as a positive assertion without any knowledge of its truth;

(3) the defendant intended to induce the plaintiff to act upon the representation;

and

(4) the plaintiff actually and justifiably relied upon the representation and suffered injury as a result.

JPMorgan Chase Bank, N.A. v. Orca Assets G.P., LLC, 546 S.W.3d 648, 653 (Tex. 2018)

(citing Ernst & Young, LLP v. Pac. Mut. Life Ins. Co., 51 S.W.3d 573, 577 (Tex. 2001)).

Importantly, Plaintiffs do not assert—or include as summary judgment evidence—any written evidence of the purported agreement to modify the loan agreement and, as such, Plaintiffs’ claims premised upon that purported modification fail under the statute of frauds.

In Texas, the statute of frauds requires that, to be enforceable, loan agreements exceeding $50,000 must be in writing and signed by the party to be bound.

TEX. BUS. & COM. CODE § 26.02;

see also Martins v. BAC Home Loans Servicing, L.P., 722 F.3d 249, 256 (5th Cir. 2013).

Such “loan agreements”

subject to the statute of frauds include promises, promissory notes, and deeds of trust.

TEX. BUS. & COM. CODE § 26.02(a)(2).

If a contract falls within the ambit of the statute of frauds, then “any subsequent oral modification to the contract” also falls within the ambit of the statute of frauds.

SP Terrace, L.P. v. Meritage Homes of Tex., LLC, 334 S.W.3d 275, 282 (Tex.App.—Houston [1st Dist.] 2010, no pet.);

see also Martins, 722 F.3d at 256

(“An agreement regarding the transfer of the property or modification of a loan must…be in writing to be valid.”).

Some oral modifications need not be in writing if they do not materially alter the obligations imposed by the original contract.

Horner v. Bourland, 724 F.2d 1142, 1148 (5th Cir. 1984).

However, “[a]n oral agreement to modify the percentage of interest to be paid, the amounts of installments, security rights, the terms of the remaining balance on the loan, the amount of monthly payments, the date of the first payment, and the amount to be paid monthly for taxes and insurance is an impermissible oral modification.”

Montalvo v. Bank of Am. Corp, 864 F. Supp. 2d 567, 582 (W.D. Tex. 2012) (citing Horner, 724 F.2d at 1148).

Here, Plaintiffs’ loan is subject to the statute of frauds because it includes a loan agreement in the original amount of $197,698.00.

See TEX. BUS. & COM. CODE § 26.02;

Martins, 722 F.3d at 256; 5:17-cv-118-DAE, docket no. 4-1 at 2.

Therefore, to be enforceable, any modification of the loan agreement would have to be in writing and signed by the party to be bound.

Martin, 722 F.3d at 256;

see also Garcia v. Wells Fargo Bank, N.A., No. SA-17-CV-747-XR, 2017 WL 4448243, at *2 (W.D. Tex. Oct. 5, 2017)

(dismissing fraud claim where promise to forestall foreclosure was not in writing);

Gordon v. JPMorgan Chase Bank, N.A., 505 F. App’x 361, 364–65 (5th Cir. 2013)

(“Although Gordon alleges that she was verbally assured that she would receive a loan modification, she does not point to a written offer to do anything more than determine her eligibility for such a modification. She therefore has not alleged facts that would allege a modification of her loan terms under the statute of frauds.”).

Plaintiffs here assert only that they were promised Defendants would consider a loan modification through their sending a modification packet to Plaintiffs.

Docket no. 22 at 6.

The record reveals that Plaintiffs have not returned any such packet to Defendants, including in March of this year when Defendants emailed another loan modification packet to Plaintiffs but had yet (as of May 12th) to receive any response.

Docket no. 20-6 at 2–3 (sending loan modification packet on March 13 and requesting completion by March 27).

Thus, even if the Court construed Defendants’ sending of the loan modification packet itself as a promise to consider Plaintiffs’ eligibility for a loan modification, Plaintiffs do “not point to a written offer to do anything more than determine [their] eligibility for such a modification” and thus, they have “not alleged facts that would allege a modification of [their] loan terms under the statute of frauds.”

Gordon, 505 F. App’x at 364–65.

Accordingly, the statute of frauds bars enforcement of the alleged promise to modify the loan agreement, and Plaintiffs’ fraud claim fails as a matter of law.

Garcia, 2017 WL 4448243, at *2

(dismissing common-law fraud claim where alleged misrepresentation was barred by the statute of frauds).

Plaintiffs’ common-law fraud claim also fails to meet the heightened pleading requirements of Rule 9(b), which requires that “a party must state with particularity the circumstances constituting fraud or mistake.”

FED. R. CIV. P. 9(b).

Plaintiffs must set forth specific facts supporting an inference of fraud, and Plaintiffs here have not done so.

Dorsey v. Portfolio Equities, 540 F.3d 333, 339 (5th Cir. 2008).

Though a promise of future performance—such as the promise to modify a loan—can support a fraud claim, “the promise complained of must have been made ‘with no intention of performing.”

Formosa Plastics Corp. v. Presidio Eng’rs and Contractors, Inc., 960 S.W.2d 41, 48 (Tex. 1998).

A promise to do an act in the future is actionable fraud only “when made with the intention, design and purpose of deceiving, and with no intention of performing the act.”

Spoljaric v. Percival Tours, Inc., 708 S.W.2d 432, 434 (Tex. 1986).

The evidence here does not reveal any such intent; rather, the evidence shows that Defendants have repeatedly sent Plaintiffs the loan remodification packet, including as recently as March of this year, and have been met with silence.

See docket no. 20-6 at 2.

The evidence of Defendants’ intentions shows no such intent to deceive or to not perform the promised act; it shows the opposite.

How to Stop Foreclosure in Texas, Even if You’ve Failed Before, or Before That.

It’s DeAcceleration for Homeowners, thanks to Federal Court Judge Ellison, Houston, Texas. @uscourts @DeutscheBank @WellsFargo @RocketMortgage @usbank @Yale @Harvard @UTexasLaw @Baylor @ACLUTx pic.twitter.com/AmzZJCN1FR

— lawsinusa (@lawsinusa) June 8, 2022

CONCLUSION

For the foregoing reasons, Defendants’ motion for summary judgment (docket no. 19) is GRANTED.

The Clerk is DIRECTED to enter judgment in favor of Defendants and against Plaintiffs.

Plaintiffs shall take nothing by their claims.

It is so ORDERED.

SIGNED this 24th day of July, 2020.

XAVIER RODRIGUEZ

UNITED STATES DISTRICT JUDGE

Fourteenth Court of Appeals: The Doctrine of Res Judicata Does Not Apply to Claims Made for the First Time

Williams’ allegations standing alone and construed in his favor do not demonstrate the HHA’s entitlement to dismissal under res judicata.

Fifth Circuit: Unclean Hands Defense by Debtor in Bankruptcy Does Not Invoke Res Judicata

Debtors unclean hands defense was not available to him in the Louisiana litigation and the state judgment fails to confirm it was litigated.

How Federal Courts Weaponized the All Writs Act to Silence Homeowners and Violate Constitutional Rights

LIT Exposes How Federal Courts Use the All Writs Act to Control Litigants and Conceal Real Estate Fraud by Bandit Lawyers and Their Clients.

{kind=link}