LIT COMMENTARY

Nov. 30, 2022

The Government National Mortgage Association (or Ginnie Mae) is a government corporation within the U.S. Department of Housing and Urban Development (HUD). It was established in 1968 when Fannie Mae was privatized. Its mission is to expand funding for mortgages that are insured or guaranteed by other federal agencies.

The Government has redesigned and relaunched both their HUD and Ginnie Mae websites, but doing so should not impinge on the data and content from the old site, which should be archived and available to all citizens.

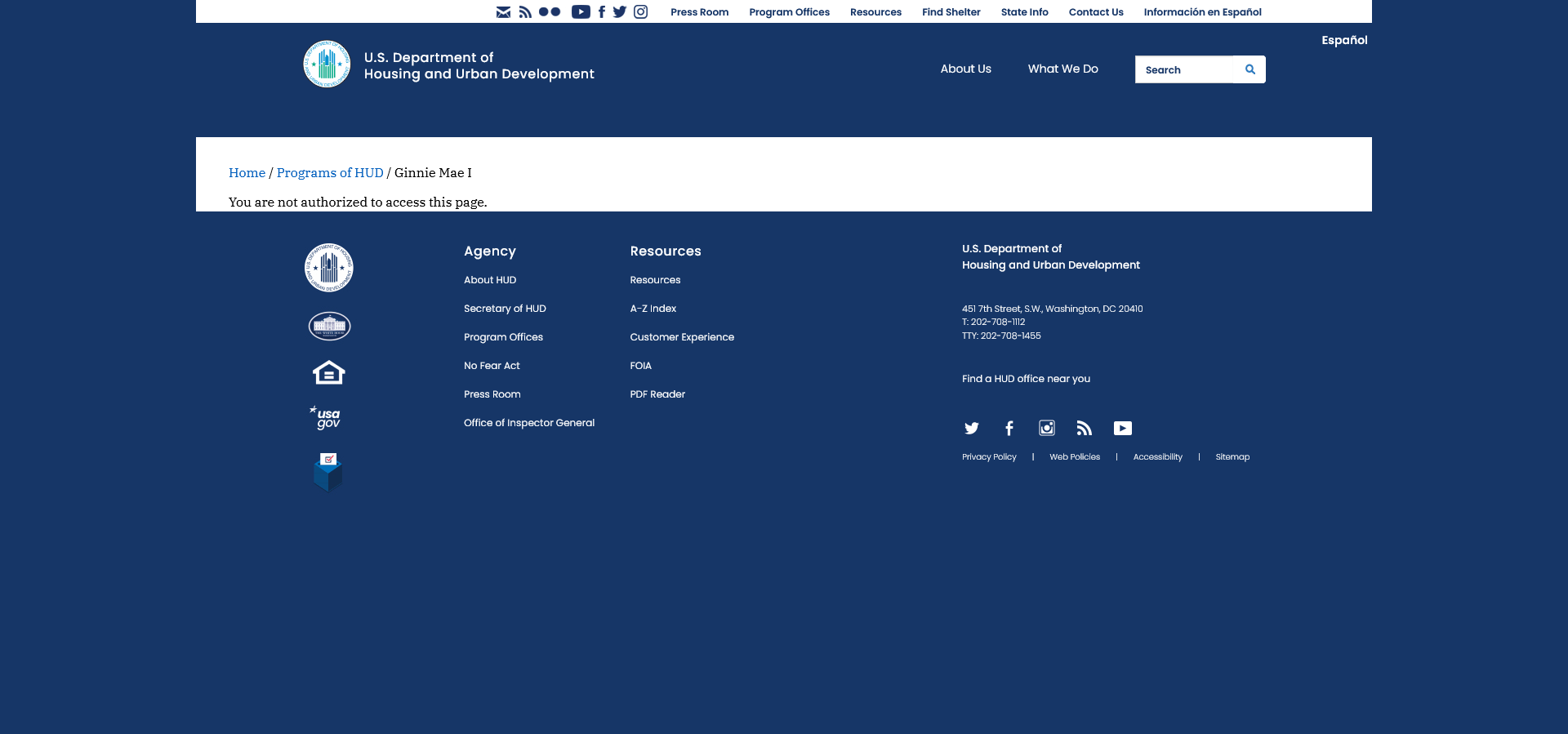

For example, the gov. have blocked this article which is shown as ‘active’ on the now archived site.

Here’s what LIT’s view of that article looks like.

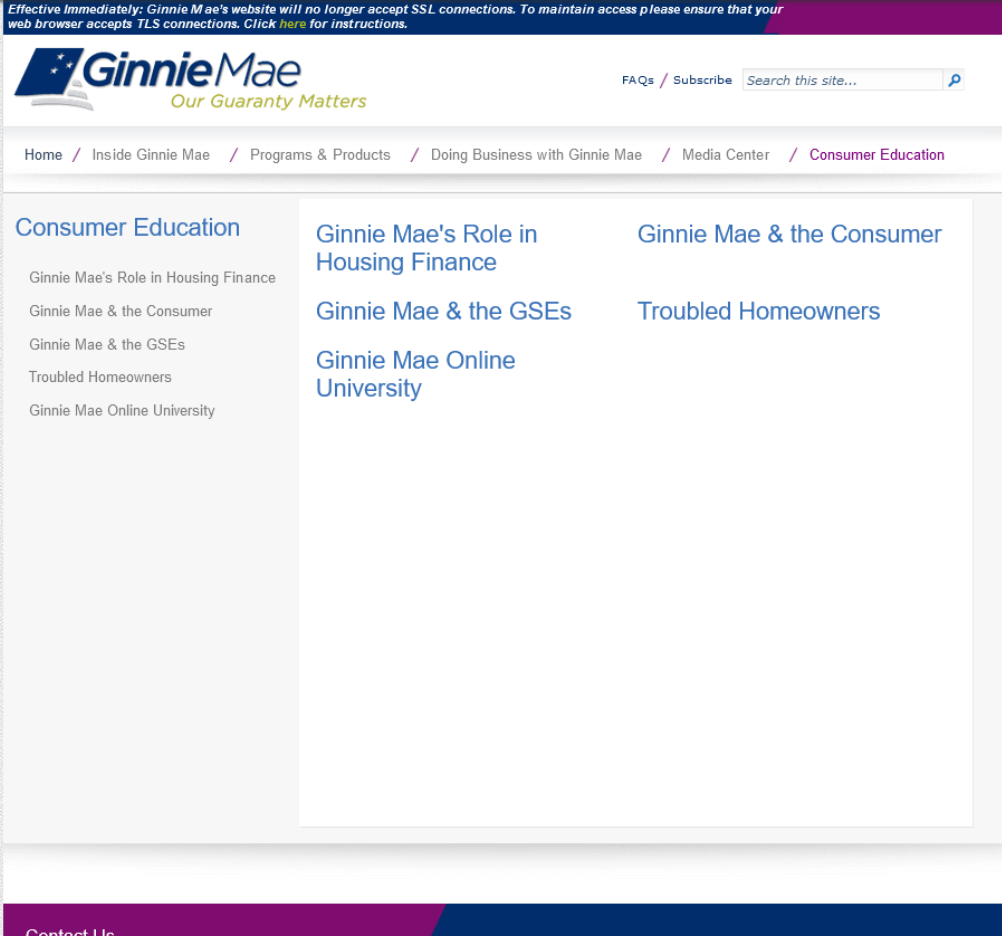

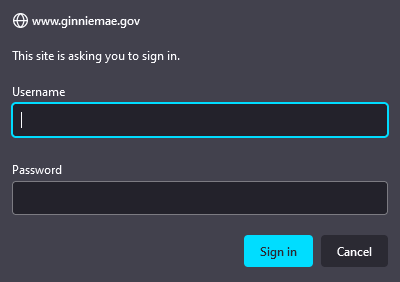

And further into the article below, what was once a ‘consumer education‘ section now requires a user login.

And looking at the visual focus of the old site for Ginnie versus the new website, it’s no longer “consumer focused“.

Who are Freddie Mac, Fannie Mae and Ginnie Mae?

Ginnie Mae exists to solely guarantee the security of the loan. Fannie Mae and Freddie Mac are regulated under the conservatorship authority of the Federal Finance Housing Agency. Fannie Mae typically buys loans from larger commercial banks.

DEC 3, 2014 | REPUBLISHED BY LIT: APR 11, 2022

Understanding mortgage loan securities.

Freddie Mac and Fannie Mae are known as Government Sponsored Enterprises, private companies that are sponsored by the US Government.

Freddie Mac and Fannie Mae are publicly-traded corporations that securitize residential mortgages and sell them to investors as mortgage-backed securities.

Freddie Mac and Fannie Mae are not government agencies, but Ginnie Mae is.

Ginnie Mae is housed within the Department of Housing and Urban Development and provides guarantees to cover loses lenders would suffer through federally insured or guaranteed loans, should a residential homeowner default on their borrower obligations.

Ginnie Mae is known as a guarantor for federally backed loans, while Fannie and Freddie guarantee loans themselves.

This means that when borrowers become delinquent on loan obligations, Fannie and Freddie are responsible for the losses on the loans they guarantee, while Ginnie Mae issuers become financially responsible for the delinquent debt.

This encourages lending institutions to be careful in selection of how and who loans are dispersed to since they may be financially responsible for the losses on a bad loan.

Ginnie Mae guarantees mortgage backed securities of those loans that are the following:

FHA-Federal Housing Administration;

VA-Veterans Affairs;

RD-Rural Development;

and

PIH-Office of Public and Indian Housing.

Fannie Mae and Freddie Mac loans are typically conventional mortgage loans.

Unlike Fannie Mae and Freddie Mac, Ginnie Mae does not participate in determining eligibility for loan modifications, make loans to potential homebuyers, purchase loans from other lenders or assist potential homebuyers with purchasing a home.

The criteria and decisions for all of the aforementioned are executed by the lender.

Ginnie Mae exists to solely guarantee the security of the loan.

Fannie Mae and Freddie Mac are regulated under the conservatorship authority of the Federal Finance Housing Agency.

Fannie Mae typically buys loans from larger commercial banks.

Freddie Mac purchases mortgage loans from smaller banks and credit unions, also known as “thrift” savings institutions.

Those loans are then pooled together and sold to investors as mortgage-backed securities.

How to Serve Ginnie Mae

If you are involved in a lawsuit as a plaintiff and have to serve your complaint on Ginnie Mae, below is a real life example of the instructions given to a pro se litigant in federal court in Houston, Texas.

April 8, 2022

Via Email and Certified Mail

David Lee Daniels, III

P.O. Box 1004

Spring, TX 77383-1004

ddaniels.science1@gmail.com

Re: Case No. 4:22-cv-00199: Daniels v. PennyMac Loan Services, LLC et al

Dear Mr. Daniels:

As explained in my email to you, service in connection with the above-referenced civil action has not been perfected on Ginnie Mae as of today, April 8, 2022.

Rule 4(i) of the Federal Rules of Civil Procedure sets forth the proper procedure for service on corporations of the United States.

Your delivery of the complaint only to Ginnie Mae does not constitute complete service of process on the United States in accordance with Rule 4(i)(1) of the Federal Rules of Civil Procedure.

The United States does not execute waivers of service under Rule 4(d).

Rule 4(i)(2) requires any suit against an agency or corporation of the United States to also be served on the United States.

To effectuate service on the United States, Rule 4(i)(1)(A) requires that a copy of a summons and the complaint be served on the United States Attorney for the district in which the action is brought.

As a temporary measure due to COVID-19 concerns, service on the United States Attorney in civil cases must be via email and U.S. mail.

A copy of any summons, complaint or emergency motion shall be emailed to USATXS.CivilNotice@usdoj.gov.

A paper copy shall be mailed to the Civil Process Clerk, United States Attorney’s Office, 1000 Louisiana Street, Suite 2300, Houston, Texas 77002.

Hand delivery may not be accepted.

Service will not be deemed effected until you receive an e-mail acknowledgement from our office.

Rule 4(i)(1)(B) also requires that a copy of the summons and complaint be served on the Attorney General of the United States by sending a copy by registered or certified mail to the Attorney General of the United States at Washington, D.C.

Note that Rule 12(a) provides the United States sixty (60) days to file an answer to the complaint after proper service, and this should be specified on the summons.

For your reference, I have included an instruction sheet that provides details on perfecting service of process.

If you have any questions relating to proper service, you may contact me at (713) 567-9600.

Please be advised that the United States and Ginnie Mae will not waive service in this action and that it is incumbent upon you to secure a summons from the clerk of the Court and secure service in the manner prescribed under the Federal Rules of Civil Procedure and temporary COVID-19 measures.

This letter shall not be construed as a waiver of service or as an appearance.

I ask that once you have perfected service, you kindly provide me a copy of the return mail receipt(s) indicating service for each person/entity.

Sincerely,

JENNIFER B. LOWERY

United States Attorney Southern District of Texas

By: /s/ Myra F. Siddiqui

Myra F. Siddiqui

Assistant United States Attorney

cc: United States District Judge George C. Hanks, Jr., via CM/ECF Enclosure

CashCall Returns To the Ninth Circuit and the Panel Discusses Equity versus Restitution, In Law

CashCall, Inc: They are to pay more than $134 million in legal restitution to which they object. The Ninth Circuit rejected their arguments.

Denied Rights? Homeowner Barred from Viewing Own PHH Loan File But US Gov Can Demand Direct Access

Federal law, the RFPA, authorizes US gov to obtain 300 PHH Mortgage loan files without notifying or obtaining the consent of any borrowers.

Mega Financial Crisis Settlement for Investors But Zero Compensation for True Victims: The Homeowners

The 2008 Scandal: DOJ admits predatory lending was responsible but settlement provides no restitution for true victims: the homeowners.

{kind=link}

{kind=link}

{kind=link}